Market talk for the week (19 April)

22 Apr 2021

What happened in markets this week, and what are analysts talking about?

Sembcorp Industries

• Credit Suisse: Initiate coverage on SCI with an OUTPERFORM rating and TP of S$2.40, based on Sum of the parts valuation implying ~1.2x FY21F P/B. SCI is shifting to renewables as it looks to grow its renewables capacity to 4,000MW (31% of its energy portfolio) by 2022 from its current ~3,300MW. According to Credit Suisse, SCI may have room to re-rate as it is trading at 0.9x P/B vs its renewable energy peers of more than 3x P/B, if SCI is able to successfully grow its renewables portfolio.

•HSBC: Upgrade SCI to BUY from HOLD, with an increased TP of $2.61 (implied 2021F P/B of 1.3x) from $1.68. HSBC now values the energy division of SCI at 8x 2021F EV/EBITDA (from 7x previously), a slight premium to the FY2021F market cap-weighted EV/EBITDA of its peers (excluding outliers) to account for SCI being the only Singapore based energy company listed on STI.

![]()

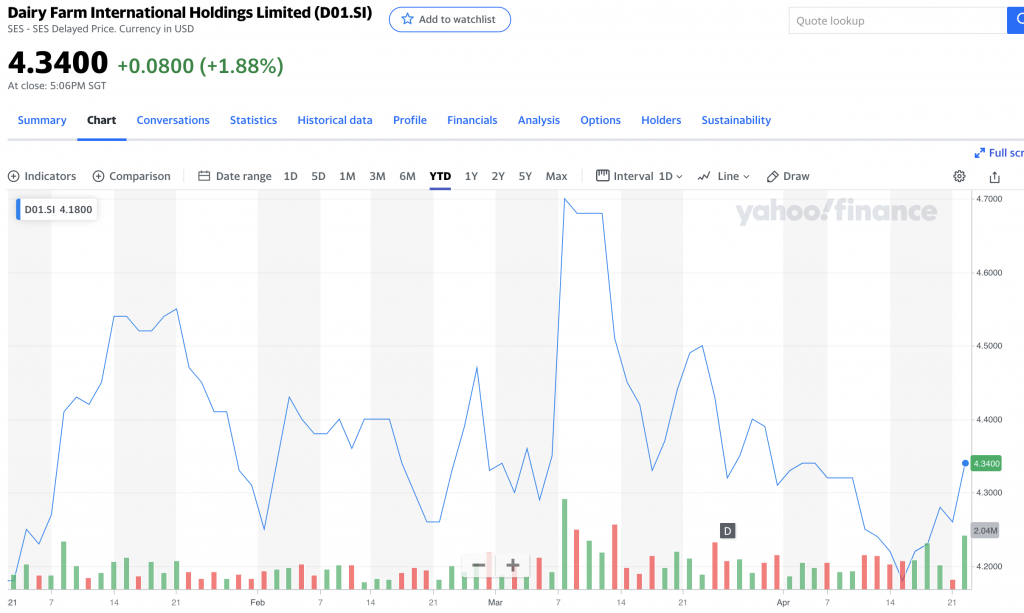

Dairy Farm International

• UOB: Initiate coverage on Dairy Farm International (DFI) with a BUY and TP of $5.19. Sees DFI as a play on Asia’s developed and emerging markets with its multiyear strategic transformation since 2018 having led to higher EBITDA margins. DFI is the largest retailer in Asia ex-Japan with a strong market presence in China, HK, Taiwan, India and ASEAN. DFI’s PE is 1SD below its 5 year average which the house thinks is undervalued due to the Group’s stable platform as the economies in the region recovers and earnings growth over the next few years.

Thai Beverage

The proposed spinoff of Thai Beverage's beer business has been deferred due to uncertain market conditions and volatile outlook. Beerco, ThaiBev's subsidiary, has 3 breweries in Thailand and interest in 26 breweries in Vietnam.

• UOB Kayhian; Lucas Teng: Thai Bev remains attractively priced at 17x FY21F PE, -1SD to its average PE. The Group's core spirits business continues to show resilience, with majority off-trade sales. The house recommend accumulating on weakness

• Maybank, Kareen Chan: Stock is trading at 15x FY21F PE, -1SD below 5 year mean and 65% discount to its peers of 45x. The house noted the increased risk for Thaibev due to the resurgence of COVID-19 in Thailand and Vietnam, as well as the absence of a catalyst from the potential spinoff. However, the house believe share price may be supported by attractive valuation

For our more info on markets and access to stock research, pls open a trading account with our preferred broker or subscribe to us. PM @moneyplantt at Telegram or email us at connect@gem-comm.com