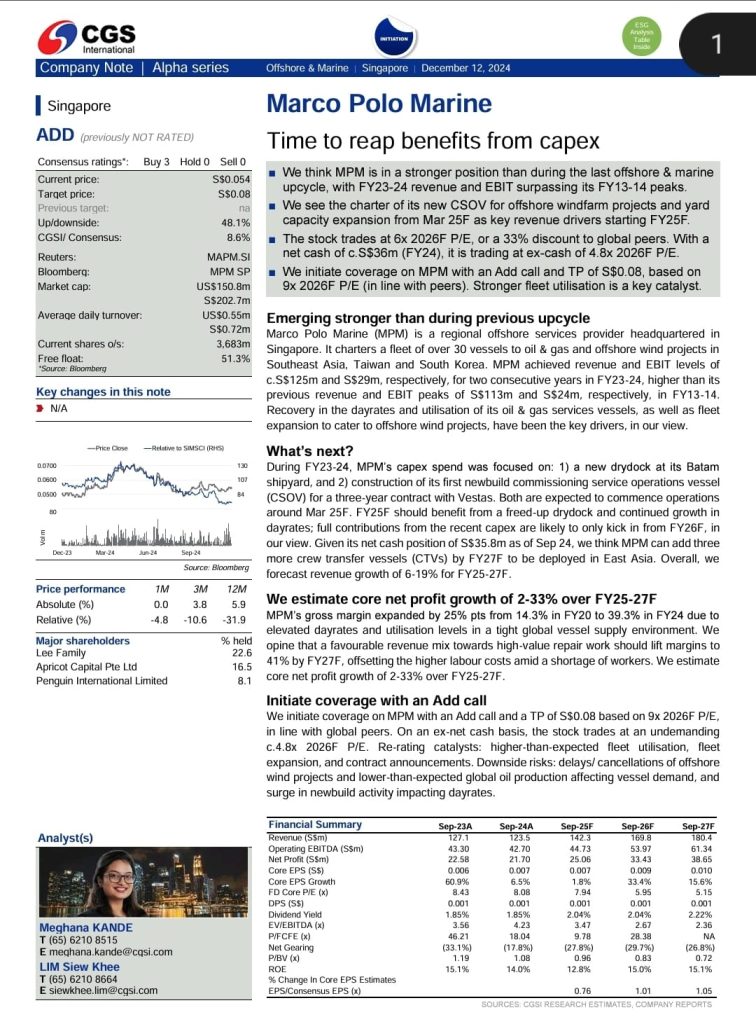

CGS Research INITIATION on MARCO POLO MARINE (SGX: 5LY)

CGS initiates coverage on MPM with an Add call and TP of S$0.08, based on

9x 2026F P/E (in line with peers). Stronger fleet utilisation is a key catalyst.

📈Time to reap benefits from capex

MPM is in a stronger position than during the last offshore & marine

upcycle, with FY23-24 revenue and EBIT surpassing its FY13-14 peaks.

The charter of its new CSOV for offshore windfarm projects and yard

capacity expansion from Mar 25F as key revenue drivers starting FY25F.

The stock trades at 6x 2026F P/E, or a 33% discount to global peers. With a

net cash of c.S$36m (FY24), it is trading at ex-cash of 4.8x 2026F P/E.

As the world transitions away from fossil fuels, offshore energy offers promising solutions to meet growing energy demands while significantly reducing our carbon footprint.

Discover the untapped potential of offshore energy and its pivotal role in shaping a sustainable future. From harnessing the power of the wind and waves to exploring ocean depth for renewable resources, the offshore energy sector is the next frontier of innovation.

Join us with our distinguished speakers from Sheffield Green, Marco Polo Marine, Mermaid Maritime, and GEM COMM, as we discuss the sector’s outlook, and how companies within the sector can benefit from the global energy transition.

Industries: Offshore wind, wave power, energy infrastructure

Featured ListCos: Marco Polo Marine, Mermaid Maritime, Sheffield Green

A reminder email will be sent one day before the event.

Dress Code: Smart Casual

RSVP: Admission is free, Registration is required

Speakers

Mr. Royston Tan – Head of Research, GEM COMM

Mr. Sean Lee Yun Feng – Chief Executive Officer, Marco Polo Marine

Mr. Bryan Kee Boo Chye – CEO, Chairman, and Executive Director, Sheffield Green

Mr. Paul Whiley – Chief Operating Officer and Executive Director, Mermaid Maritime

Programme

Time

Session

6.30pm

Registration

7.00pm

Market/Sector Outlook – Mr. Royston Tan, Head of Research, GEM COMM

7.20pm

Harnessing the Power of Wind: Marco Polo Marine’s Commitment to a Sustainable Future – Mr. Sean Lee Yun Feng, CEO of Marco Polo Marine

7.35pm

Unlocking the Depths: How Mermaid Maritime is Driving Efficiency in Subsea Operations – Mr. Paul Whiley, COO and Executive Director of Mermaid Maritime

7.50pm

Fuelling the Renewable Energy Future: Sheffield Green’s Leadership in Global HR Solutions – Mr. Bryan Kee Boo Chye, CEO, Chairman, and Executive Director of Sheffield Green

8.05pm

Panel Discussion + Combined Q&A

8.30pm

End of Programme

*Sessions and timings may be subject to change.

This event may be subject to audio and video recording and photography, which SGX may use for internal and external publicity, and share with participants for commemorative purposes.

By providing my personal information herewith, I consent and authorize Singapore Exchange Limited (“SGX”) and/or its affiliates (collectively with SGX, the “SGX Group Companies”) to process, collect, use, disclose and store the information I have provided (including personal data) for security checks & monitoring in relation to SGX’s premises or premises managed by SGX and contacting me for emergency purposes.

Please visit SGX Privacy Policy for information on SGX’s data protection policy.

PhillipCapital is upbeat on local co-living operator LHN, as the research house has kept its “buy” call, while raising target price to 42 cents from 39 cents previously.

Analyst Paul Chew says: “We raised our FY2024 earnings by 7% to account for the better-than-expected earnings from Coliwoo… We expect growth to remain stable for LHN in 2HFY2024, supported by stable room rates.”

Chew’s high expectations of the stock comes on the back of its latest 1HFY2024 ended March results announcement, which saw revenue increase by 27.2% y-o-y to $57.5 million, driven by the group’s co-living business, which saw revenue doubled and earnings tripled. Earnings dropped by 23.4% y-o-y to $13.0 million.

The commencement of the 411 keys in Coliwoo Orchard in February 2023 was a major boost to room rates. The residential rental index in Singapore is up 33% over the past two-years but has started to stabilise.

The group’s profit before tax declined 25.0% y-o-y to $15.3 million. Further removing the effect of fair value loss, gain on disposal of associate and discontinued operations from the logistics group, the group would have recorded a 13.7% y-o-y growth in 1HFY2024 adjusted profit before tax to $17.7 million, compared to $15.6 million in 1HFY2023.

Revenue came in within Chew’s expectations, but earnings had exceeded. “Revenue and adjusted PATMI were 51%/65% of our FY2024 forecast, respectively. Margins for co-living were higher than expected due to the high occupancy and room rates,” says Chew.

The way Chew sees it, FY2025 will be a banner year of growth for LHN. The number of keys in co-living will expand by at least 900 (187 in Coliwoo GSM Building and 700 healthcare professionals).

After a stellar rise in residential rents of 50% over the past three years, rents have started to move sideways. Nevertheless, Chew sees that the demand for co-living remains healthy. Demand is now coming from corporate accounts, as Coliwoo focus its marketing efforts on this segment.

Co-living is still more than 50% cheaper than hotels and still provides services (housekeeping) and amenities (cooking, laundry, broadband) to its residents. Another driver is the increased number of residents in the country. In 2023, the population rose by 281,000 to 5.91 million, the highest annual increase on record and 6x the pre-pandemic average of 47,000. LHN targets to grow co-living by 800 keys every year.

In addition, the sale of 49 food processing industrial units will be another one-off gain from the property development business.

The Coliwoo franchise is also scaling up and expanding into third party management contracts. The stock pays a dividend yield of 6% and trades at a P/E of 5.2x and 40% discount-to-book value of 55 cents.

On the other hand, Chew is cautious on the group’s weaker facilities management earnings, which saw a 32% y-o-y decline to $1.7 million despite revenue growth of 14% y-o-y to $17.2 million. The number of car parks under management rose from 74 (about 20,000 lots) to 81 (about 25,000 lots). “We believe the margin weakness was due to a loss of government grants. Nevertheless, the number of car park lots will grow with the recent contract award of another 900 car park lots,” says Chew.

Shars in LHN closed 3% higher on May 23 at 34 cents.

Unlock the Power of Global Investor Relations! 🌐💼

At Gem Comm, we bridge the communication gap for companies with a global footprint, like our client Procurri – listed on SGX since 2016 and with a CEO based in the US. 🇸🇬🇺🇸

𝗣𝗿𝗼𝗰𝘂𝗿𝗿𝗶’𝘀 𝗠𝗿 𝗝𝗼𝗿𝗱𝗮𝗻 underscores the importance of tapping Gem Comm’s familiarity with the nuances of SGX and the local investor community. This strategic partnership allows Procurri to better articulate its messaging and vision with clarity, transcending geographical boundaries even while Mr Jordan leads from the US.

Gem Comm’s expertise lies in seamlessly connecting businesses with their investors, no matter where they are. We help listed clients like Procurri uphold the highest reporting and disclosure standards while fostering close communication channels on the ground.

By leveraging on our tailored investor relations strategies, we cultivate trust, nurture enduring connections, and unlock lasting value for companies and their stakeholders alike.

Trust Gem Comm to be your global investor relations partner – we can elevate your business to new heights while keeping your investors engaged and informed every step of the way! 🚀🌍

Li Jialin and Eric Ong of Maybank Securities have kept their “buy” call and 45 cents target price for LHN after the co-living operator announced it is adding two new developments to its portfolio.

First, LHN won a government tender for the former Bukit Timah fire station, which will be refurbished at a cost of $7 million to become a mixed-use project with 60 serviced apartment units on levels 2 & 3, and a ground floor commercial F&B and retail operation.

According to LHN, this site will serve as a key community node for both the Rail Corridor and the surrounding precinct and is expected to be open by June 2025.

“In our view, the Bukit Timah project should capitalize on LHN’s expertise and synergy across its business units in co-living, commercial and facility management,” write Li and Ong in their April 11 note.

Meanwhile, LHN is also teaming up with Oxley Holdings 5UX 0.00% CEO Ching Chiat Kwong and his son Shawn Ching in a 50-50 joint venture to acquire Wilmer Place, which is at 50 Armenian Street, near the City Hall MRT.

According to the Maybank analysts, the office building could remain as a commercial building or be re-purposed for LHN’s co-living business.

With a land area of 710.7 sqm, the leasehold building has a tenure of 99 years from 1 May 1947. This should enable the LHN, which is spending up to $24 million for this project, to expand its co-living offerings under its space optimization business segment.

In total, LHN has 6 upcoming projects, including the Ministry of Health hostel for 700 nursing professionals.

To help fund this growth, LHN is offering commercial paper of up to $5 million, at a 6% interest rate

With MOH proposing another 11 other sites, this suggests possible re-rating catalysts for LHN if it can secure more of these projects, according to the Maybank analysts.

Their target price of 45 cents is pegged at 8 times forward FY2024 earnings.

LHN shares changed hands at 34 cents as at 2.05pm, up 1.52% for the day.

Acquisition of BK Aesthetics Clinic at 100AM Mall, Tanjong Pagar

Consideration of S$117,026 based on independent asset valuation and share exchange at S$0.015 per piece

SINGAPORE, 11 April 2024 – Beverly JCG Ltd. (SGX: 9QX) (the “Beverly JCG” or

the “Company”, and together with its subsidiaries, the “Group”), a reputable brand in

Malaysia, together with Beverly Wilshire (“BW”), a multi-award-winning integrated

beauty and wellness medical group specialising in cosmetic surgery, aesthetic medicine,

general and specialist dental aesthetics, hair restoration and a range of healthy ageing

and wellness services, wishes to announce that on 9 April 2024, the Company has

entered into a sale and purchase agreement to acquire BK Aesthetics Clinic located at

#04-11 and #04-12, 100AM, 100 Tras Street, Singapore, to enhance the Group’s

portfolio in the healthcare and wellness sector.

The acquisition, settled through a share exchange valued at S$0.015 per share,

underscores Beverly JCG’s investment in regional growth and expansion. By

incorporating BK Aesthetics Clinic into its portfolio, Beverly JCG is setting a strong

foundation for growth through a foray into Singapore and signals its intention to explore

further acquisition opportunities. This initiative aligns with the company’s broader

objective to become a leading regional player in healthcare, wellness, and beauty.

Dato’ Ng Tian Sang, Deputy Chairman and CEO, stated, “This transformative acquisition marks a pivotal step in our ambition to establish Beverly JCG as the preeminent force in the region’s healthcare, beauty, and wellness industry. We remain committed to pursuing growth opportunities that will propel us to new heights, solidifying our position as a trusted provider of unparalleled value to our clients and shareholders.”

Beverly JCG’s acquisition of BK Aesthetics Clinic marks the start of its ambitious journey

to dominate the healthcare, wellness, and beauty industry in the region. The company

promises innovative solutions and exceptional service quality to its clientele.

Dyna-Mac Holdings has secured several contracts, bringing its order book to a new high of $896 million. These projects will be delivered till 2026.

The main contract involves the construction of process modules. It marks the largest-ever contract win in Dyna-Mac’s history, involving a record tonnage and number of process modules in a single contract.

The rest of the contracts include the provision of services for the execution, fabrication, installation and integration work on vessels, and scope increase for current projects.

According to Dyna-Mac, its recent capacity expansion and upgrading allows for the further optimization of construction methodology and production workflow. This will increase Dyna-Mac’s productivity in that it’ll use lesser manpower and time needed for the same amount of work.

The new orders are not expected to have a material impact on Dyna-Mac’s earnings per share (EPS) and net tangible assets (NTA) for the FY2024 ending Dec 31.

Shares in Dyna-Mac closed 1.5 cents higher or 4% up at 39 cents on April 2.

The ASEAN region, like the rest of the world, has seen a significant boom in the digital economy thanks to the rapid adoption of digital technologies and services by consumers and businesses during the COVID-19 pandemic.

According to the e-Conomy SEA report by Google, Temasek, and Bain & Company, Southeast Asia’s digital economy exceeded US$190 billion in gross merchandise value (GMV) in 2022 and is expected to grow at double digits to reach U295 billion by 2025.

Digital adoption continues to rise post-pandemic, with key sectors such as e-commerce, transportation and food, travel and online media fueling this growth.

On this note, monetization has gained momentum across the region over the last two years where the region’s revenue is expected to grow at a rate 1.7x higher than that of GMV. The emphasis on monetization is motivated by the quest for financial sustainability and improved unit economics across various sectors.

Multiple growth drivers to foster swift adoption

According to the Bloomberg 2021 report, ASEAN possesses the world’s most rapidly expanding mobile wallet market. The upswing in cross-border trade over the past decade has played a pivotal role in driving the adoption of digital payments.

Historically, cross-border transactions were linked to high costs and prolonged processing times. However, digital payments have now emerged as a convenient and efficient solution to overcome these challenges.

In fact, a recent global study, conducted in partnership with Juniper Research, predicts a staggering 311% growth in the number of mobile wallets used across Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam from 2020 to nearly 440 million by 2025.

A PWC report also shared about how “consumers are swiftly embracing digital financial services, signaling a shift away from the era where cash reigned supreme”.

According to a recent report by Google, Temasek, and Bain & Company, digital payments now constitute over 50% of transactions in the region.

In certain areas like Southeast Asia, the prevalence of digital payments through e-wallets has already surpassed physical card payments and is poised to become the predominant method across point-of-sale systems overall,” noted Dan Jones and Alex Walker of OliverWyman.

As technology continues to reshape the financial landscape, ASEAN nations are also embracing innovative solutions to cater to the evolving needs of consumers and businesses alike.

For instance, to support the development and integration of digital payments in the region, 5 ASEAN central banks – Bank Indonesia, Bank Negara Malaysia, Bangko Sentral ng Pilipinas, Monetary Authority of Singapore (MAS), and Bank of Thailand – have signed a cooperation agreement to establish an interoperable cross-border payment system that will allow instant and seamless digital transactions across ASEAN countries.

The system will use QR codes as a common standard for digital payments, enabling users to scan and pay with their preferred mobile wallets or apps. The system will also facilitate remittances and e-commerce transactions, as well as reduce the reliance on cash and the U.S. dollar.

Tapping on the digital payments’ revolution

As the ASEAN digital payments industry continues to flourish, savvy investors are eyeing opportunities to benefit from this upward trajectory.

One way is to invest in the companies who have secured digital banking licenses in Singapore to provide banking services entirely online, without any physical branches.

As of 2023, there are 4 digital banks in Singapore:

· GXS Bank (consortium backed by Grab Holdings and Singtel)

· MariBank (owned by SEA Limited)

· Anext Bank (backed by Ant Group – Alipay)

· Green Link Digital Bank (consortium involving Greenland Financial, Linklogis Hong Kong, and Beijing Co-operative Equity Investment Fund Management)

Digital banks help to streamline tedious financial processes and offer various advantages for customers and merchants, such as convenience, efficiency and cost-effectiveness.

For example, GXS Bank, a consortium backed by Grab Holdings and Singtel, leverages its existing ecosystem of ride-hailing, food delivery, e-commerce, and mobile payments to offer seamless and integrated banking solutions for its users and partners.

Green Link Digital Bank, backed by Greenland Financial Holdings, intends to use its experience in real estate, logistics, and trade finance to offer cross-border payment and lending solutions for SMEs in Singapore and China.

Another direct way that investors can tap on the digital payment revolution is through Oxpay Financial, a payment solutions provider that offers online and offline payment services in Singapore and abroad.

Oxpay Financial operates a payment gateway platform that connects merchants with various payment methods such as credit cards, e-wallets and bank transfers. Given its presence in the 4 ASEAN countries Singapore, Malaysia, Indonesia, and Thailand, Oxpay emerges as an attractive investment option for those seeking exposure to the growing digital finance market in ASEAN.

You can read more about Oxpay Financial’s tie-up with GLDB here.

Conclusion

With the ASEAN digital banking and payment systems industry undergoing a remarkable transformation, Oxpay Financial, with its innovative solutions and strategic approach, stands out. Oxpay Financial is poised to play a pivotal role in shaping the future of digital payments in ASEAN.

The shift towards digital payments in ASEAN is not just a fad; it’s a structural shift fueled by technological advancements and changing consumer behaviors.

As the financial landscape continues to evolve and digitalise, this trend will create many promising investment opportunities for those looking to capitalize on the digital finance boom in the ASEAN region.

The construction scene in Singapore took a hard hit from the COVID-19 pandemic. Supply chains got all tangled up, projects were delayed, and the demand for new developments dropped like a brick (pun intended).That being said, the industry is showing signs of recovery and rejuvenation, thanks to the solid backing from the government’s projects and the resilience of the industry players.In this article, we will highlight the underlying trends that will shape the sector and Singapore’s construction industry outlook in the foreseeable future.

4 Leading Construction Trends

The construction sector was among Singapore’s worst-hit industries during the pandemic. The slow productivity in construction work was largely due to substantial labour shortages amid ongoing border restrictions and implementation of stringent safety measures.

Consequently, Singapore’s heavy reliance on low-cost foreign labour for its construction sector has spurred a heightened urgency for construction businesses to integrate digital solutions, fostering adaptability and enhancing efficiency and productivity.

On top of that, in accordance with the new policy – Singapore Green Plan 2030, the government has pinpointed sustainability as a primary focus within the built environment sector.

Accordingly, four prominent trends are poised to mold the industry in the medium and long term. These encompass:

1. A growing demand for green buildings, manifested through the adoption of eco-friendly building solutions, such as smart sensors for monitoring water and energy usage.

2. A mounting emphasis on efficient construction practices, with the government advocating for the adoption of the Design for Manufacturing and Assembly methodology. This involves designing construction for off-site manufacturing before final assembly on-site.

3. A shift towards more inclusive designs, ensuring that the built environment accommodates individuals with diverse needs. Addressing the design requirements for an aging population holds particular significance, given that over a third of Singapore’s population is projected to be over 65 years old by 2035.

4. Increased incorporation of smart technology through the utilization of Integrated Digital Delivery (IDD). This approach leverages digital technologies to seamlessly integrate work processes and connect stakeholders involved in the same project throughout the construction and building phases.

In a nutshell, the Singapore authorities maintains an ongoing emphasis on sustainable practices, with the implementation of regulations pertaining to the use of prefabrication elements, decarbonization, redevelopment, and environmental protection and management at construction sites.

Breakdown of Construction Projects Pipeline

According to a media release, the Building and Construction Authority (BCA) projected that contracts totaling between $27 billion and $32 billion are likely to be awarded in 2023 – similar to what was observed in the past two years.

The private-sector construction demand is anticipated to be between the range of $11 billion to $13 billion, mirroring the figures from 2022. This projection is tied to the scheduled development of new condominiums and high-specification industrial buildings.

On the other hand, an estimated 60 percent of the overall construction demand for year 2023 is anticipated to come from the public sector, amounting to a range between $16 billion and $19 billion. This is attributed to the upcoming projects such as Build-To-Order (BTO) flats, MRT lines, and water treatment plants.

In the medium term, the Building and Construction Authority (BCA) envisions the annual total construction demand to come in between $25 billion and $32 billion from 2024 to 2027.

During this period, the public sector expects to sustain its ~60% lead in demand, with upcoming projects such as the Cross Island Line and several hospital developments.

Simultaneously, private sector construction demand is anticipated to remain steady, with an annual expected range of approximately S$11 billion to S$14 billion from 2024 to 2027. This outlook is underpinned by robust investment commitments, supported by the resilient economic fundamentals of Singapore.

Building a Comeback

The construction industry in Singapore is poised for stability in the coming years, thanks to various factors such as the digitilisation measures to improve efficiency, Singapore Green Plan 2030 and many more infrastructure projects.

For construction firms that have faced financial challenges, particularly in the aftermath of the COVID-19 pandemic, this phase of stability marks a promising beginning for a potential revival. The sector’s ability to withstand adversity, coupled with a steady influx of projects, creates fertile ground for these companies to bounce back and, subsequently, transform into profitable entities.

Below we ‘drill’ into some of the construction-related stocks in Singapore…

A quick glance shows that most of them are trading below 1x their book values and have below $100 million market capitalization. On top of that, many of them are still sitting near their 52 weeks low despite the recovery of the construction sector – something that investors can take notice of.

Now, let’s shine the spotlight on three stocks in the list:

Firstly, Tiong Seng Holdings Limited is a construction company in Singapore that has recently announced its intention to sell its leasehold property located at 510 Thomson Road for S$10 million.

Given that the proposed disposal is considered a major transaction under the SGX regulations, an extraordinary general meeting (EGM) was convened on 15 December 2023 and the ordinary resolution passed with flying colours (99% approval).

The company has stated that the rationale for the proposed disposal is to unlock the value of the property and to improve its cash flow and financial position. The company also intends to use the net proceeds from the proposed disposal for its general working capital purposes and/or to fund its business expansion plans.

Next up is BRC Asia – a construction company in Singapore that provides steel reinforcement solutions for various projects, such as buildings, bridges, and tunnels.

The company has state-of-the-art facilities and capabilities, such as the use of digitalisation, automation, and prefabrication technologies. The company also has a strong commitment to sustainability, as it supports the Singapore Green Plan 2030 and adopts green and smart features and standards in its projects.

BRC Asia’s orderbook remains robust, standing at S$1.3 billion as of end 4Q FY2023. It remains a strong proxy for Singapore’s construction sector, given its lion’s market share domestically.

Lastly, we have Sin Heng Machinery, one of the leading heavy lifting service providers in Singapore. The company has a fleet of cranes and aerial lifts that it rents out and trades and it also sells and distributes spare parts for the equipment that it deals with.

The majority of its orderbook is derived from the Land Transport Authority (LTA) and Public Utilities Board (PUB) and these government contracts are longer term and provide good orderbook visibility.

It also possesses a strong financial position with only a meager 0.9% debt/equity ratio and has been on an active shares buyback spree from September to November 2023.

Conclusion

In conclusion, Singapore’s construction industry is currently positioned for stability and expansion after the lessons learnt from the COVID-19 pandemic. With a focus on sustainability, digitalization measures, and a robust pipeline of infrastructure projects, the sector presents promising prospects.

This positive outlook is particularly beneficial for construction companies aiming to recover from temporary financial setbacks including the ones we cover: Tiong Seng Holdings, BRC Asia, and Sin Heng Machinery. While the construction sector may be perceived as dull and uneventful, its underlying stability and consistent demand make it a worthwhile area for investors to explore further.

The company achieved a net profit of US$3.5 million, marking a significant turnaround from the loss of US$0.15 million in the preceding year. Gross margins also expanded from 15.8% to 28.0% during the same period – leading to a 528.3% Y-o-Y jump in gross profits to US$7.7 million.

This impressive growth is underpinned by a substantial 255% increase in revenue from US$7.7 million in FY2022 to US$27.6 million in FY2023, attributed to more contracts secured in the offshore wind industry.

The icing on the cake is the proposal of a final dividend of S$0.01 per share, less than 2 months after its IPO on 30 October 2023.

A quick look at its balance sheet shows that its debt/equity ratio stands at a paltry 8.9% so paying a dividend is no issue at all.

Navigating the Winds of Change

The company attributes its robust performance to the escalating demand for renewable energy initiatives, particularly in the offshore wind sector, where Sheffield Green holds a competitive advantage.

According to IRENA, employment in the renewable energy sector is expected to surge from 12.7 million in 2021 to 38.2 million by 2030.

After experiencing relatively flat spending between 2015 and 2020, investments in renewable energy, encompassing both private capital and public expenditure, increased significantly from USD 348 billion in 2020 to USD 499 billion in 2022, marking a substantial 43% growth. The majority of these funds were allocated to the solar and wind industries, with their collective share of total renewable energy investments escalating from 82% in 2013 to an impressive 97% in 2022.

In addition, Precedence Research estimates that the offshore wind sector is projected to grow from USD 33.0 billion in 2022 to USD 179.4 billion by 2032.

Hence, the company’s primary focus on offshore wind projects is well-timed, as the sector’s expansion is anticipated to catalyse substantial job opportunities in the renewable energy industry in the long run.

Company’s Growth Momentum

In its press release, the Group shared several initiatives to capitalise on these thriving industry trends namely:

Offering comprehensive human resource solutions

Sourcing for diverse roles from C-suite to technical and offshore crew positions

Provision of ancillary services such as meticulous handling of visa and work permit applications

To further strengthen its regional presence, the Group is strategically expanding into other international markets by establishing local offices. Notably, the Poland office commenced operations in November 2023, and plans are underway for the establishment of a US regional office in Boston.

Building on the success of its training centres in Taiwan, the Group envisions opening more training centres in markets like Japan and Poland to meet the escalating global demand for renewable energy personnel.

Bryan Kee, CEO of Sheffield Green, conveyed confidence in the FY2023 results with these comments:

“Reflecting on this transformative year, I am immensely proud of our team’s achievements. Our success in FY2023 is a direct result of the team’s relentless commitment, adaptability, and innovative strategies in the renewable energy sector.

Despite the challenging economic environment, we have not only managed to achieve significant growth but also enhanced our operational efficiencies and strengthened our market position. This success is a testament to our dedicated team and the solid partnerships we have fostered. We are excited to continue this momentum and further our mission of powering sustainable energy solutions.”

Peer Valuations

Based on the peer valuations chart above, Sheffield Green is trading at a relatively cheaper valuation compared to its global listed peers. The company has a price-to-earnings ratio of 8.9x, which is significantly lower than the industry average of 19x.

Some of the more renowned staffing players such as Manpower Group, Kelly Services and Singapore’s own HRnet Group have much higher P/E ratios of 17.4x, 31.4x and 11.1x respectively.

On top of that, Sheffield Green’s competitive edge in the renewable energy sector may be a stronger growth driver for its earnings going forward. This means that the company may be an attractive investment opportunity in the renewable energy staffing industry.

Conclusion

The Group’s strategic penetration into flourishing offshore wind markets in Taiwan, Japan, and Poland, coupled with its emphasis on workforce development, underscores its strong investment potential amid the burgeoning opportunities in the renewable (offshore wind) energy sector.

Be sure to ‘catch the wind’ as the Group navigates and capitalises on the rising momentum of renewable energy staffing solutions!