The construction scene in Singapore took a hard hit from the COVID-19 pandemic. Supply chains got all tangled up, projects were delayed, and the demand for new developments dropped like a brick (pun intended).That being said, the industry is showing signs of recovery and rejuvenation, thanks to the solid backing from the government’s projects and the resilience of the industry players.In this article, we will highlight the underlying trends that will shape the sector and Singapore’s construction industry outlook in the foreseeable future.

4 Leading Construction Trends

The construction sector was among Singapore’s worst-hit industries during the pandemic. The slow productivity in construction work was largely due to substantial labour shortages amid ongoing border restrictions and implementation of stringent safety measures.

Consequently, Singapore’s heavy reliance on low-cost foreign labour for its construction sector has spurred a heightened urgency for construction businesses to integrate digital solutions, fostering adaptability and enhancing efficiency and productivity.

On top of that, in accordance with the new policy – Singapore Green Plan 2030, the government has pinpointed sustainability as a primary focus within the built environment sector.

Accordingly, four prominent trends are poised to mold the industry in the medium and long term. These encompass:

1. A growing demand for green buildings, manifested through the adoption of eco-friendly building solutions, such as smart sensors for monitoring water and energy usage.

2. A mounting emphasis on efficient construction practices, with the government advocating for the adoption of the Design for Manufacturing and Assembly methodology. This involves designing construction for off-site manufacturing before final assembly on-site.

3. A shift towards more inclusive designs, ensuring that the built environment accommodates individuals with diverse needs. Addressing the design requirements for an aging population holds particular significance, given that over a third of Singapore’s population is projected to be over 65 years old by 2035.

4. Increased incorporation of smart technology through the utilization of Integrated Digital Delivery (IDD). This approach leverages digital technologies to seamlessly integrate work processes and connect stakeholders involved in the same project throughout the construction and building phases.

In a nutshell, the Singapore authorities maintains an ongoing emphasis on sustainable practices, with the implementation of regulations pertaining to the use of prefabrication elements, decarbonization, redevelopment, and environmental protection and management at construction sites.

Breakdown of Construction Projects Pipeline

According to a media release, the Building and Construction Authority (BCA) projected that contracts totaling between $27 billion and $32 billion are likely to be awarded in 2023 – similar to what was observed in the past two years.

The private-sector construction demand is anticipated to be between the range of $11 billion to $13 billion, mirroring the figures from 2022. This projection is tied to the scheduled development of new condominiums and high-specification industrial buildings.

On the other hand, an estimated 60 percent of the overall construction demand for year 2023 is anticipated to come from the public sector, amounting to a range between $16 billion and $19 billion. This is attributed to the upcoming projects such as Build-To-Order (BTO) flats, MRT lines, and water treatment plants.

In the medium term, the Building and Construction Authority (BCA) envisions the annual total construction demand to come in between $25 billion and $32 billion from 2024 to 2027.

During this period, the public sector expects to sustain its ~60% lead in demand, with upcoming projects such as the Cross Island Line and several hospital developments.

Simultaneously, private sector construction demand is anticipated to remain steady, with an annual expected range of approximately S$11 billion to S$14 billion from 2024 to 2027. This outlook is underpinned by robust investment commitments, supported by the resilient economic fundamentals of Singapore.

Building a Comeback

The construction industry in Singapore is poised for stability in the coming years, thanks to various factors such as the digitilisation measures to improve efficiency, Singapore Green Plan 2030 and many more infrastructure projects.

For construction firms that have faced financial challenges, particularly in the aftermath of the COVID-19 pandemic, this phase of stability marks a promising beginning for a potential revival. The sector’s ability to withstand adversity, coupled with a steady influx of projects, creates fertile ground for these companies to bounce back and, subsequently, transform into profitable entities.

Below we ‘drill’ into some of the construction-related stocks in Singapore…

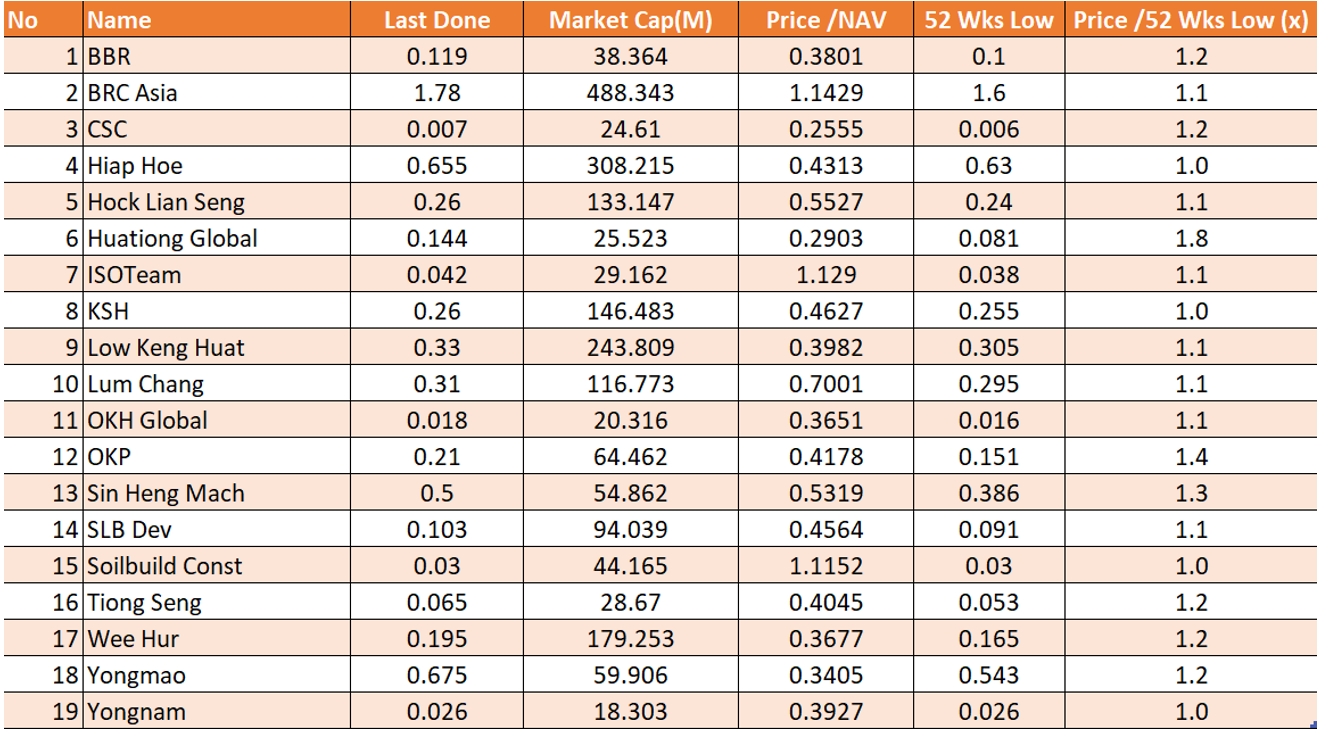

A quick glance shows that most of them are trading below 1x their book values and have below $100 million market capitalization. On top of that, many of them are still sitting near their 52 weeks low despite the recovery of the construction sector – something that investors can take notice of.

Now, let’s shine the spotlight on three stocks in the list:

Firstly, Tiong Seng Holdings Limited is a construction company in Singapore that has recently announced its intention to sell its leasehold property located at 510 Thomson Road for S$10 million.

Given that the proposed disposal is considered a major transaction under the SGX regulations, an extraordinary general meeting (EGM) was convened on 15 December 2023 and the ordinary resolution passed with flying colours (99% approval).

The company has stated that the rationale for the proposed disposal is to unlock the value of the property and to improve its cash flow and financial position. The company also intends to use the net proceeds from the proposed disposal for its general working capital purposes and/or to fund its business expansion plans.

Next up is BRC Asia – a construction company in Singapore that provides steel reinforcement solutions for various projects, such as buildings, bridges, and tunnels.

The company has state-of-the-art facilities and capabilities, such as the use of digitalisation, automation, and prefabrication technologies. The company also has a strong commitment to sustainability, as it supports the Singapore Green Plan 2030 and adopts green and smart features and standards in its projects.

BRC Asia’s orderbook remains robust, standing at S$1.3 billion as of end 4Q FY2023. It remains a strong proxy for Singapore’s construction sector, given its lion’s market share domestically.

Lastly, we have Sin Heng Machinery, one of the leading heavy lifting service providers in Singapore. The company has a fleet of cranes and aerial lifts that it rents out and trades and it also sells and distributes spare parts for the equipment that it deals with.

The majority of its orderbook is derived from the Land Transport Authority (LTA) and Public Utilities Board (PUB) and these government contracts are longer term and provide good orderbook visibility.

It also possesses a strong financial position with only a meager 0.9% debt/equity ratio and has been on an active shares buyback spree from September to November 2023.

Conclusion

In conclusion, Singapore’s construction industry is currently positioned for stability and expansion after the lessons learnt from the COVID-19 pandemic. With a focus on sustainability, digitalization measures, and a robust pipeline of infrastructure projects, the sector presents promising prospects.

This positive outlook is particularly beneficial for construction companies aiming to recover from temporary financial setbacks including the ones we cover: Tiong Seng Holdings, BRC Asia, and Sin Heng Machinery. While the construction sector may be perceived as dull and uneventful, its underlying stability and consistent demand make it a worthwhile area for investors to explore further.

Operating in four countries – Singapore, Malaysia, Indonesia, and Thailand, OxPay Financial Limited offers a range of payment solutions such as mobile wallets, QR code payments and cross-border remittances.The company’s focus on servicing merchants in the retail, transportation, and F&B industries through a fully integrated online-to-offline (“O2O”) platform has recently manifested in a strategic collaboration with Green Link Digital Bank Pte. Ltd. (GLDB).

A Quick Recap on Digital Banks – GLDB

Digital banks in Singapore have revolutionized the financial sector, delivering customers a fresh and accessible banking experience. The emergence of these digital banks has reshaped the banking landscape, with the Monetary Authority of Singapore (MAS) granting licenses to four distinct digital banks in 2020:

On this note, Green Link Digital Bank (GLDB) is held by a consortium involving Greenland Financial, Linklogis Hong Kong, and Beijing Co-operative Equity Investment Fund Management.

These banks provide a diverse array of banking services, ranging from virtual banking to digital wealth management, catering specifically to the market’s needs.

While Digital Full Banks are allowed to take deposits from retail customers, Digital Wholesale Banks like ANEXT and GLDB can only target non-retail segments i.e. providing banking services that cater to the monetary needs of small and medium-sized enterprises (SMEs).

And this is where OxPay and GLDB can collaborate in a win-win partnership.

OxPay and GLDB’s Partnership

In a press release dated 21 December 2023, OxPay announced a Memorandum of Understanding (MOU) with GLDB, aimed at exploring opportunities in merchant acquisition, with both companies leveraging their strengths to achieve mutual business expansion goals.

Under the terms of the MOU, OxPay’s subsidiary, OxPay SG Pte. Ltd., will actively promote GLDB’s banking and financing facilities within its growing merchant network.

In return, GLDB will be sharing OxPay’s cutting-edge payment solutions to its existing customer base – potentially increasing the base of prospective merchants and business entities for OxPay.

This strategic move underscores OxPay’s dedication to creating synergies within the financial technology sector, bringing together payment solutions and digital banking services for the benefit of clients and merchants.

Mr Yick Li Tsin, Chief Operating Officer of OxPay SG, commented,

“By combining OxPay’s robust payment solutions with GLDB’s specialised banking services, we are setting a new standard for integrated financial services. Our collaboration is not just about business growth, but also aims to create synergies to drive significant value for our customers and the market.”

Mr Gary Wu, Chief Marketing Officer of GLDB, added,

“As a digital bank, our financial services are naturally readily accessible. However, we have also ensured that we make it simpler, safer, and more rewarding for SMEs to obtain financial services from our collaboration with OxPay.”

Benefits from Growing ASEAN Payments Industry

The collaboration between OxPay and GLDB comes at a pivotal time for the ASEAN payments industry.

According to a report by Google, Temasek, and Bain & Company, the Asean payments industry is expected to reach US$1.3 trillion by 2025. The report also forecasts that digital payments will account for 40% of total payments in Southeast Asia by 2025, up from 10% in 2020, driven by the rapid adoption of e-commerce, online travel, and ride-hailing services, as well as the increasing penetration of smartphones and internet access.

With that in mind, the ASEAN market presents immense potential for companies operating in the payments and banking sectors. The integration of OxPay’s payment solutions with GLDB’s digital banking services bodes well for OxPay to capitalize on the burgeoning opportunities within the region.

OxPay’s Insider Ownership Emits Confidence

Another positive sign for OxPay’s investors is the high level of insider ownership and buying activity.

Chairman Mr. Ching Chiat Kwong – who is also CEO of Oxley Holdings – owns 27.8% of the company’s shares, indicating a strong alignment of interests with shareholders.

In addition, according to the latest filings, Mr. Ching has been actively buying more shares in the open market over the past year. This shows that Mr. Ching is confident and optimistic about the company’s prospects and performance, as well as his commitment to creating long-term value for shareholders.

Conclusion

In conclusion, OxPay Financial Limited’s collaboration with Green Link Digital Bank marks a strategic confluence of payment solutions and digital banking services.

Investors may find this collaboration promising, considering the potential for increased revenue streams, expansion of market share, and a strengthened position in the competitive financial technology landscape.

The company achieved a net profit of US$3.5 million, marking a significant turnaround from the loss of US$0.15 million in the preceding year. Gross margins also expanded from 15.8% to 28.0% during the same period – leading to a 528.3% Y-o-Y jump in gross profits to US$7.7 million.

This impressive growth is underpinned by a substantial 255% increase in revenue from US$7.7 million in FY2022 to US$27.6 million in FY2023, attributed to more contracts secured in the offshore wind industry.

The icing on the cake is the proposal of a final dividend of S$0.01 per share, less than 2 months after its IPO on 30 October 2023.

A quick look at its balance sheet shows that its debt/equity ratio stands at a paltry 8.9% so paying a dividend is no issue at all.

Navigating the Winds of Change

The company attributes its robust performance to the escalating demand for renewable energy initiatives, particularly in the offshore wind sector, where Sheffield Green holds a competitive advantage.

According to IRENA, employment in the renewable energy sector is expected to surge from 12.7 million in 2021 to 38.2 million by 2030.

After experiencing relatively flat spending between 2015 and 2020, investments in renewable energy, encompassing both private capital and public expenditure, increased significantly from USD 348 billion in 2020 to USD 499 billion in 2022, marking a substantial 43% growth. The majority of these funds were allocated to the solar and wind industries, with their collective share of total renewable energy investments escalating from 82% in 2013 to an impressive 97% in 2022.

In addition, Precedence Research estimates that the offshore wind sector is projected to grow from USD 33.0 billion in 2022 to USD 179.4 billion by 2032.

Hence, the company’s primary focus on offshore wind projects is well-timed, as the sector’s expansion is anticipated to catalyse substantial job opportunities in the renewable energy industry in the long run.

Company’s Growth Momentum

In its press release, the Group shared several initiatives to capitalise on these thriving industry trends namely:

Offering comprehensive human resource solutions

Sourcing for diverse roles from C-suite to technical and offshore crew positions

Provision of ancillary services such as meticulous handling of visa and work permit applications

To further strengthen its regional presence, the Group is strategically expanding into other international markets by establishing local offices. Notably, the Poland office commenced operations in November 2023, and plans are underway for the establishment of a US regional office in Boston.

Building on the success of its training centres in Taiwan, the Group envisions opening more training centres in markets like Japan and Poland to meet the escalating global demand for renewable energy personnel.

Bryan Kee, CEO of Sheffield Green, conveyed confidence in the FY2023 results with these comments:

“Reflecting on this transformative year, I am immensely proud of our team’s achievements. Our success in FY2023 is a direct result of the team’s relentless commitment, adaptability, and innovative strategies in the renewable energy sector.

Despite the challenging economic environment, we have not only managed to achieve significant growth but also enhanced our operational efficiencies and strengthened our market position. This success is a testament to our dedicated team and the solid partnerships we have fostered. We are excited to continue this momentum and further our mission of powering sustainable energy solutions.”

Peer Valuations

Based on the peer valuations chart above, Sheffield Green is trading at a relatively cheaper valuation compared to its global listed peers. The company has a price-to-earnings ratio of 8.9x, which is significantly lower than the industry average of 19x.

Some of the more renowned staffing players such as Manpower Group, Kelly Services and Singapore’s own HRnet Group have much higher P/E ratios of 17.4x, 31.4x and 11.1x respectively.

On top of that, Sheffield Green’s competitive edge in the renewable energy sector may be a stronger growth driver for its earnings going forward. This means that the company may be an attractive investment opportunity in the renewable energy staffing industry.

Conclusion

The Group’s strategic penetration into flourishing offshore wind markets in Taiwan, Japan, and Poland, coupled with its emphasis on workforce development, underscores its strong investment potential amid the burgeoning opportunities in the renewable (offshore wind) energy sector.

Be sure to ‘catch the wind’ as the Group navigates and capitalises on the rising momentum of renewable energy staffing solutions!

James Yeo: “Can you provide a detailed overview of Beverly JCG Ltd’s (BJCG) evolution and strategic transformations since its inception, particularly focusing on the key acquisitions and expansions and explain how these moves align with the company’s vision of becoming a major player in the aesthetic and healthcare industry in the region?”Dato’ Ng: “BJCG has undergone several strategic shifts and significant acquisitions. It was established as Albedo Limited in 2005 as an industrial products trading company before it ventured into the healthcare sector by investing in China Medical (International) Group Limited (CMIG) in 2016. In January 2019, the company was renamed JCG Investment Holdings Ltd.”In Nov 2019, it acquired 51% of Beverly Wilshire (BW) group of companies, which operates a branded chain of aesthetics medicine, plastic surgeries, dental clinics, and regenerative stem cell medicine, including hair transplants in Malaysia in Kuala Lumpur, Klang Valley and Pelating Jaya, Bangsar, Ipoh and Johor Bahru.

The Ng family, headed by myself, was the controlling shareholder of BW group, with key doctors as my shareholders. BJCG recently acquired two aesthetic and beauty spa clinics, including Dr BK Kim, in 100 AM Mall Amara Hotel in Tanjong Pagar Singapore CBD. This will start our first foray into Singapore and will contribute Singapore revenue to BJCG.

This will also position BJCG as a regional player in aesthetic medicine and have Singapore as our business headquarters. We are also cautiously venturing into Indonesia, Vietnam, and China via mergers & acquisitions (M&As) to augment the company’s profit.

Recently, BJCG acquired the balance of 49% of BW Group, ensuring the shareholders’ goals and objectives are fully aligned. This acquisition is a significant milestone for the company and shall further strengthen the BW brand in Singapore and the region to make the BW brand a household word.

The decision to list the company’s shares in Singapore was strategic, leveraging Singapore as a centre of medical excellence and its reputation as an international financial centre. Through these transformations and strategic decisions, the company’s aim has always been clear – to become a major player in the aesthetic and healthcare industry in the region.”

James Yeo:

“How has BJCG’s financial performance evolved post-acquisition, and what strategies are being implemented to maintain profitability and expand growth opportunities, particularly in Malaysia and regionally?”

Dato’ Ng:

“BJCG recorded a revenue of about S$10.5 million in FY2022. Despite the global pandemic, BW made its maiden profit in 2021, particularly through our Malaysian operations.

We aim to solidify our regional presence and explore new profitable avenues, maintaining a strong performance while embracing growth opportunities.”

James Yeo:

“Could you explain the rationale and strategic significance behind the 50:1 share consolidation and how this move enhances the company’s market appeal, share liquidity, and overall financial strategy in preparation for future growth initiatives?”

Dato’ Ng:

“The share consolidation, at 50:1 (consolidating every 50 ordinary shares into one ordinary share), will reduce the issued shares from 29.1 billion to about 582.2 million. This is a strategic move to enhance our market appeal and improve the share liquidity and volatility.

It’s a step to recalibrate our share structure, making our stock more attractive and meaningful to investors. This consolidation is part of a broader strategy to fortify our financial foundation and prepare for future growth initiatives.”

James Yeo:

“Can you elaborate on the structure and objectives of the Rights Cum Warrants Issue at a 3:1 ratio, particularly in the context of the recent share consolidation, and explain how this initiative aims to attract investment and support BJCG’s growth strategies?”

Dato’ Ng:

“In our recent Rights Cum Warrants Issue, structured at a 3:1 ratio following the share consolidation, we’ve set an advantageous issue price of S$0.035 per Rights Share, a significant reduction from the initially announced S$0.05. This new issue price is strategically placed at a 30% discount to the post-consolidation last traded price of S$0.05 per Share and about 24% below the theoretical ex-rights price of S$0.046 per Share.

We’re offering free detachable Rights Warrants with an exercise price of S$0.051 for each Warrant Share, compared to the previously announced S$0.06. This exercise price represents a modest 2% premium over the post-consolidation last traded price and is approximately 10% higher than the theoretical ex-rights price.

These adjusted prices for both the Rights Shares and the Warrants are designed to enhance the appeal of our offering to investors, aligning with our strategic goal of bolstering BJCG’s growth and expansion, particularly in the wake of our recent share consolidation. We believe this initiative is pivotal in attracting investment and fortifying our market position.”

James Yeo:

“Could you describe BJCG’s philosophy and approach towards service and safety in the healthcare sector, and how does this ethos contribute to the company’s distinction in the competitive aesthetic market?”

Dato’ Ng:

“We are a branded, fully integrated healthcare outfit. And our philosophy is that we always provide the Best 5-star services and practice safety first.”

James Yeo:

“Could you discuss how investors may underappreciate the share consolidation and Rights Cum Warrants Issue in terms of their potential to enhance the company’s market dynamics and attract strategic long-term investment, especially considering your growth projections from 2024 onwards?”

Dato’ Ng:

“Some investors may not fully recognise BJCG’s growth potential. Our share consolidation and subsequent Rights Cum Warrants Issue are geared towards creating a more dynamic market for our shares and attracting long-term, strategic investors.

By setting an attractive post-consolidation Rights share base price, good M&As, and a well-defined strategic alliances plan, BJCG will do better from 2024 onwards.”

James Yeo:

“As BJCG navigates its strategic initiatives and market developments, what message would you like to convey to our readers about the company’s direction, its approach to creating stakeholder value, and the opportunities it presents for investors in its ongoing transformation and growth?”

Dato’ Ng:

“While share consolidation often leads to initial market reactions, we are confident about our strategic direction. We have several key initiatives underway that should positively influence our stakeholders’ value.

Our approach goes beyond mere market trends; we are actively shaping our future with a clear strategic vision, a dedicated team, and a commitment to growth. BJCG represents a solid investment choice and a journey of transformation and success.”

Established in 1991, Marco Polo Marine is an integrated marine logistics company that provides a wide range of services to the offshore oil and gas, and renewable energy sectors.

The company has reported a strong performance for its financial year ended 30 September 2023 (FY2023). In this article, we will zoom into its financial results, growth prospects, valuation and more.

Powered By Twin Growth Engines

Marco Polo Marine operates 2 main business segments:

1) Ship Chartering Division relating to the chartering of Offshore Supply Vessels (OSVs), tugboats and charters, and

2) Shipyard Division relating to shipbuilding and provision of ship maintenance, repair, outfitting, and conversion services.

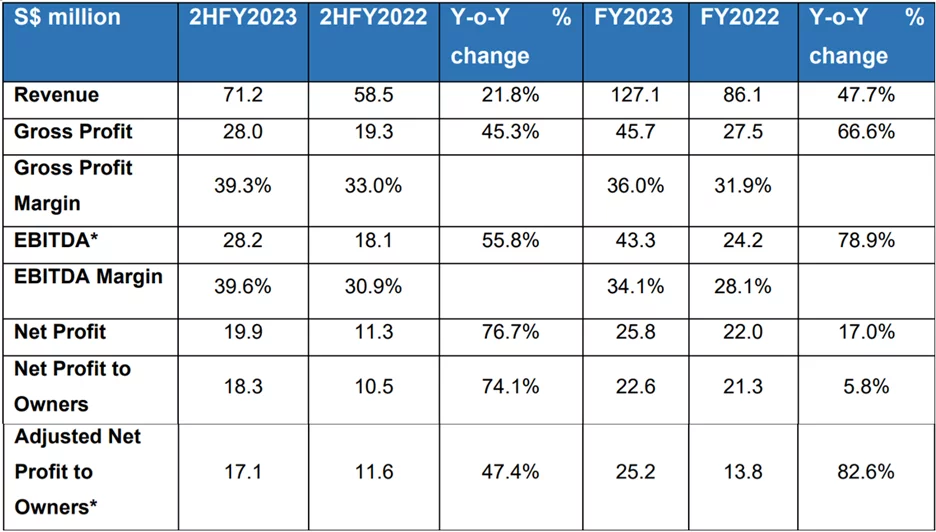

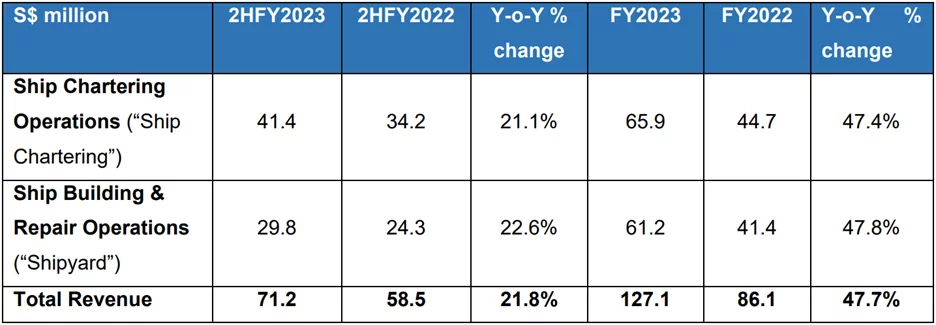

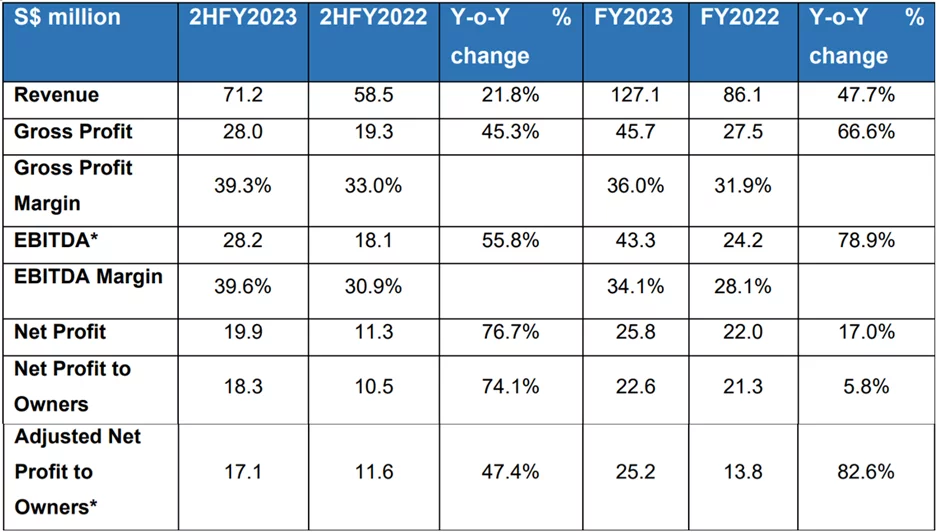

For FY2023, Ship Chartering revenue experienced a significant 47.4% year-on-year jump to S$65.9 million from S$44.7 million in the previous year.

The principal factor contributing to this boost was the complete consolidation of PT Bina Buana Raya (“PT BBR”) and PKR Offshore’s (“PKRO”) results in the ongoing financial year, as opposed to the partial consolidation in FY2022. It’s noteworthy that PT BBR and PKRO officially became subsidiaries of the Group in March and May 2022, respectively.

To add on, the revenue from Shipyard segment also exhibited a stellar 47.8% year-on-year increase to S$61.2 million as compared to the previous year, driven by higher contract values associated with repair projects and the initiation of new ship-building projects.

Consequently, Marco Polo Marine reported a substantial 78.9% year-on-year growth in EBITDA to reach S$43.3 million, underpinned by the higher revenue and better gross profit margins.

Excluding FX gains/losses and one-off items, the group’s adjusted net profit to owners saw a spectacular 82.6% jump from S$13.8 million in FY2022 to S$25.2 million in FY2023.

With that in mind, Marco Polo Marine is a leading integrated marine logistics group The company operates in Singapore, Indonesia, Malaysia, and other parts of Southeast Asia, and has been listed on the Singapore Exchange since 2007.

Stellar Growth Prospects

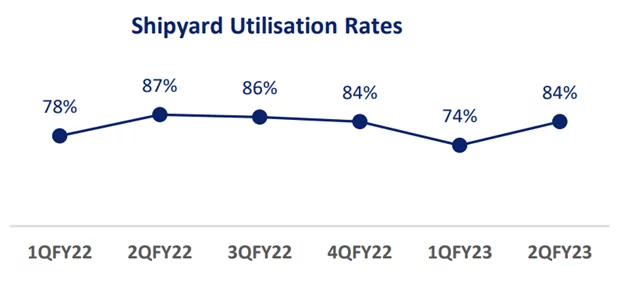

For the Shipyard business, the growth continues to be propelled by elevated contract values for ship repair projects and the securing of contracts to build several barges with progressive deliveries up to 2HFY2024.

The shipyard’s average utilisation rate stands at 84% in the 2Q FY2023 and has remained relatively stable in the past year as well.

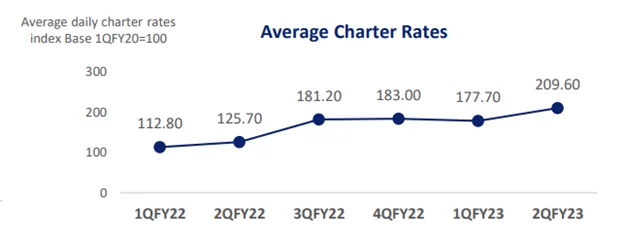

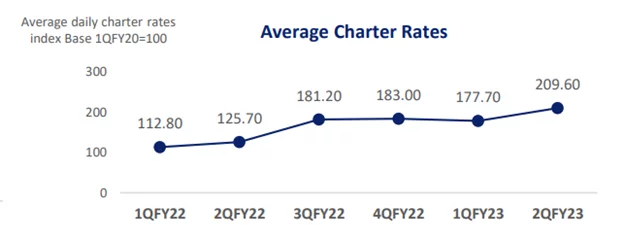

For the Ship Chartering business, revenue growth has surged due to higher vessel utilisation and increased charter rates.

As seen from the chart above, average charter rates have climbed steadily from 112.80 points in 1Q FY2022 to 209.60 points in 2Q FY2023.

The trend for the ship chartering segment of Marco Polo Marine is positive, as the company expects to see sustained demand for its vessels, especially in the Asia’s offshore wind farm sector, which is expected to grow rapidly in the coming years.

On this note, Marco Polo Marine has established a strong presence in the offshore windfarm division through its partnership with Oceanic Crown Offshore Marine Services Ltd. and by acquiring PKR Offshore Co. Ltd.

The Group has also been securing significant opportunities in the offshore wind farm sector and has achieved notable milestones, including:

Building its inaugural Commissioning Service Operation Vessel (CSOV), slated for completion in the first quarter of 2024.

Establishing a Memorandum of Understanding (MOU) with Vestas Taiwan for the CSOV’s charter.

Venturing into the Japanese market with a groundbreaking MOU signed with “K” Line Wind Service, Ltd (KWS).

Making its debut in the South Korean market through MOUs with Namsung Shipping Co., Ltd. (Namsung) and HA Energy Co., Ltd. (HA-E) on January 11, 2023.

According to marketsandmarkets.com, the global offshore wind farm market was valued at US$31.8 billion in 2021, and is projected to reach US$56.8 billion by 2026, registering a compound annual growth rate (CAGR) of 12.3% from 2021 to 2026. This bodes well for the company.

To top it off, things are also picking up in the oil and gas markets, and this is expected to boost the charter rates for their offshore support vessels in the coming financial year.

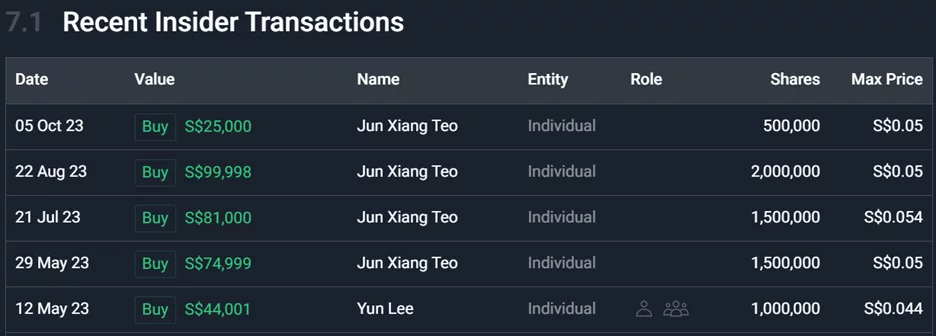

Notable Recent Purchases by Company Insiders

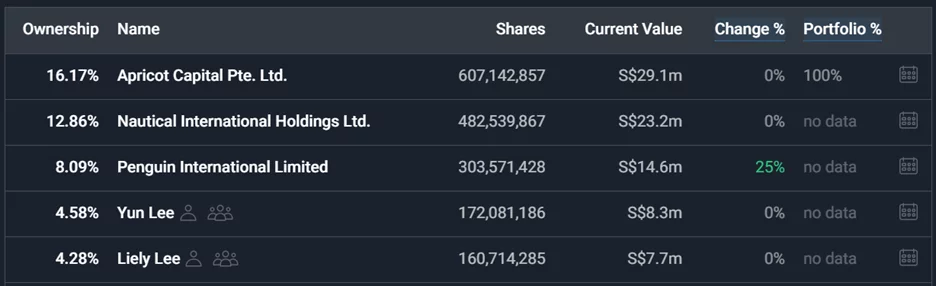

In the year 2023 itself, we have 2 notable recent purchases from 2 individuals. Mr. Yun Lee, CEO of the firm, has acquired 1 million shares from the open market on 12 May 2023.

On top of that, Mr. Teo Jun Xiang, Non-Executive Director and Managing Partner of family office Apricot Capital, has been on an acquisition spree, snapping up a total of 5.5 million shares in the past year.

What’s worth noting is that his purchase prices are all above 5 Singapore cents, which means shareholders are getting a bigger bang for their buck since the stock is trading at S$0.048 at the time of writing.

Furthermore, Apricot Capital and CEO Mr. Yun Lee own a sizable 16.17% and 4.58% stake in Marco Polo Marine respectively, which gives them the incentive to grow the business because they have the biggest vested interest of all.

Valuation backed by hard assets

As of 30 September 2023, the Group is also sitting on a cash balance of S$63.1 million. Deducting the total borrowings of S$2.3 million, it equates to a strong net cash position of S$60.8 million.

This provides the Group with the financial flexibility to continue expanding its footprint in the thriving offshore wind farm market. On top of that, the company wishes to celebrate this achievement by rewarding shareholders with a dividend of S$0.001 per share, equivalent to an estimated 2.1% dividend yield.

In addition, the Group’s valuation is also primarily backed by hard assets including cash, OSVs and its Batam shipyard. As of 30 September 2023, the Group has a net asset value of S$0.043 per share, translating into a Price/Book of 1.1x.

Conclusion

In conclusion, Marco Polo Marine has demonstrated a robust FY2023 performance with its top- and bottom-line increasing double digits on a year-to-year basis.

We can also see how the expansion into offshore windfarm markets in Asia and recent insider purchases underscore confidence in the company’s prospects.

As the company continues to navigate the dynamic marine logistics landscape, investors can look forward to potential value creation and sustained growth.

Established in 1991, Marco Polo Marine is an integrated marine logistics company that provides a wide range of services to the offshore oil and gas, and renewable energy sectors.

The company has reported a strong performance for its financial year ended 30 September 2023 (FY2023). In this article, we will zoom into its financial results, growth prospects, valuation and more.

Powered By Twin Growth Engines

Marco Polo Marine operates 2 main business segments:

1) Ship Chartering Division relating to the chartering of Offshore Supply Vessels (OSVs), tugboats and charters, and

2) Shipyard Division relating to shipbuilding and provision of ship maintenance, repair, outfitting, and conversion services.

For FY2023, Ship Chartering revenue experienced a significant 47.4% year-on-year jump to S$65.9 million from S$44.7 million in the previous year.

The principal factor contributing to this boost was the complete consolidation of PT Bina Buana Raya (“PT BBR”) and PKR Offshore’s (“PKRO”) results in the ongoing financial year, as opposed to the partial consolidation in FY2022. It’s noteworthy that PT BBR and PKRO officially became subsidiaries of the Group in March and May 2022, respectively.

To add on, the revenue from Shipyard segment also exhibited a stellar 47.8% year-on-year increase to S$61.2 million as compared to the previous year, driven by higher contract values associated with repair projects and the initiation of new ship-building projects.

Consequently, Marco Polo Marine reported a substantial 78.9% year-on-year growth in EBITDA to reach S$43.3 million, underpinned by the higher revenue and better gross profit margins.

Excluding FX gains/losses and one-off items, the group’s adjusted net profit to owners saw a spectacular 82.6% jump from S$13.8 million in FY2022 to S$25.2 million in FY2023.

With that in mind, Marco Polo Marine is a leading integrated marine logistics group The company operates in Singapore, Indonesia, Malaysia, and other parts of Southeast Asia, and has been listed on the Singapore Exchange since 2007.

Stellar Growth Prospects

For the Shipyard business, the growth continues to be propelled by elevated contract values for ship repair projects and the securing of contracts to build several barges with progressive deliveries up to 2HFY2024.

The shipyard’s average utilisation rate stands at 84% in the 2Q FY2023 and has remained relatively stable in the past year as well.

For the Ship Chartering business, revenue growth has surged due to higher vessel utilisation and increased charter rates.

As seen from the chart above, average charter rates have climbed steadily from 112.80 points in 1Q FY2022 to 209.60 points in 2Q FY2023.

The trend for the ship chartering segment of Marco Polo Marine is positive, as the company expects to see sustained demand for its vessels, especially in the Asia’s offshore wind farm sector, which is expected to grow rapidly in the coming years.

On this note, Marco Polo Marine has established a strong presence in the offshore windfarm division through its partnership with Oceanic Crown Offshore Marine Services Ltd. and by acquiring PKR Offshore Co. Ltd.

The Group has also been securing significant opportunities in the offshore wind farm sector and has achieved notable milestones, including:

Building its inaugural Commissioning Service Operation Vessel (CSOV), slated for completion in the first quarter of 2024.

Establishing a Memorandum of Understanding (MOU) with Vestas Taiwan for the CSOV’s charter.

Venturing into the Japanese market with a groundbreaking MOU signed with “K” Line Wind Service, Ltd (KWS).

Making its debut in the South Korean market through MOUs with Namsung Shipping Co., Ltd. (Namsung) and HA Energy Co., Ltd. (HA-E) on January 11, 2023.

According to marketsandmarkets.com, the global offshore wind farm market was valued at US$31.8 billion in 2021, and is projected to reach US$56.8 billion by 2026, registering a compound annual growth rate (CAGR) of 12.3% from 2021 to 2026. This bodes well for the company.

To top it off, things are also picking up in the oil and gas markets, and this is expected to boost the charter rates for their offshore support vessels in the coming financial year.

Notable Recent Purchases by Company Insiders

In the year 2023 itself, we have 2 notable recent purchases from 2 individuals. Mr. Yun Lee, CEO of the firm, has acquired 1 million shares from the open market on 12 May 2023.

On top of that, Mr. Teo Jun Xiang, Non-Executive Director and Managing Partner of family office Apricot Capital, has been on an acquisition spree, snapping up a total of 5.5 million shares in the past year.

What’s worth noting is that his purchase prices are all above 5 Singapore cents, which means shareholders are getting a bigger bang for their buck since the stock is trading at S$0.048 at the time of writing.

Furthermore, Apricot Capital and CEO Mr. Yun Lee own a sizable 16.17% and 4.58% stake in Marco Polo Marine respectively, which gives them the incentive to grow the business because they have the biggest vested interest of all.

Valuation backed by hard assets

As of 30 September 2023, the Group is also sitting on a cash balance of S$63.1 million. Deducting the total borrowings of S$2.3 million, it equates to a strong net cash position of S$60.8 million.

This provides the Group with the financial flexibility to continue expanding its footprint in the thriving offshore wind farm market. On top of that, the company wishes to celebrate this achievement by rewarding shareholders with a dividend of S$0.001 per share, equivalent to an estimated 2.1% dividend yield.

In addition, the Group’s valuation is also primarily backed by hard assets including cash, OSVs and its Batam shipyard. As of 30 September 2023, the Group has a net asset value of S$0.043 per share, translating into a Price/Book of 1.1x.

Conclusion

In conclusion, Marco Polo Marine has demonstrated a robust FY2023 performance with its top- and bottom-line increasing double digits on a year-to-year basis.

We can also see how the expansion into offshore windfarm markets in Asia and recent insider purchases underscore confidence in the company’s prospects.

As the company continues to navigate the dynamic marine logistics landscape, investors can look forward to potential value creation and sustained growth.

Property management operator LHN Limited (“LHN”) offers space optimisation solutions, property development, facilities management and energy services in Singapore and other Asian countries.

The Group currently has 4 main business segments, namely:

Space Optimisation

Property Development

Facilities Management

Energy

It has announced its FY2023 results ended 30 September 2023 and declared a final and special dividend in FY2023. On top of that, LHN announced that from it is moving from the Catalist board to the Mainboard of the SGX-ST on 13 December 2023.

With this in mind, here are 7 things investors should know about the company.

1. Growth driven by Co-living Brand Coliwoo

According to the latest FY2023 results, the Group’s main source of revenue and key driver of growth comes from the Space Optimisation Business, constituting 64.5% of the Group’s total revenue.

Revenue generated from this business segment saw a year-on-year increase of 46.1%, reaching S$60.4 million in FY2023, as compared to S$41.4 million in FY2022.

As seen from the table above, the Group’s residential properties managed a total of 2,064 keys as of September 2023, primarily fuelled by Coliwoo’s co-living business.

The ongoing renovation projects for 404 Pasir Panjang, as well as 48 and 50 Arab Street, are progressing as planned and are anticipated to contribute to the co-living business’s performance in FY2024.

In FY2023, the occupancy rates for key Coliwoo projects within the Group remained robust. Coliwoo Orchard reported an occupancy level of 93%, while Coliwoo Lavender and Coliwoo 298 River Valley achieved occupancy rates of 86% and 100%, respectively, as of September 2023.

Singapore’s co-living industry continues to thrive, driven by a confluence of factors that include surging rents and prices in the broader residential property market, higher adoption of hybrid work, as well as accelerating demand for flexible housing options by locals and expatriates, including singles and young couples.

2. Newly Added 4th Business Segment – Energy

In FY2023, the new Energy Business made its maiden contribution. This sector offers renewable energy services to industrial clients, encompassing electricity supply, the installation of solar power systems, and the provision of electric vehicle (“EV”) charging stations.

The firm has successfully deployed solar panels in 3 internal and 6 external locations throughout FY2023. Despite this segment representing only a small 0.5% share of the Group’s overall revenue, it is profitable from the onset – achieving an adjusted segmental profit of S$0.4 million for the same year.

3. Healthy Revenue and Operating Cashflow Growth

The Group experienced an 10.9% Y-o-Y increase in total revenue from continuing operations to S$93.6 million due to a broad-based growth in all business segments.

In contrast, net profit attributable to equity holders was down 16.6% to S$38.2 million over the same period, primarily due to net fair value losses amounting to S$8.7 million, as compared to a sharp fair value gains in FY2022 of S$24.8 million.

One should also note that the FY2023 net profit comprises of a gain of S$19.7 million following the successful divestment of LHN Logistics Limited and its affiliated companies (referred to as the “Logistics Group”) on 28 August 2023. The Logistics Services Business segment will no longer contribute to the Group’s performance from the next financial year onwards.

On a bright note, net cash generated from operating activities increased from S$41.2 million in FY2022 to S$54.2 million in FY2023, underpinned by enhanced working capital management.

4. Improving Balance Sheet

As of 30 September 2023, the net gearing ratio of the Group decreased to 43.6% compared to 44.5% a year ago, largely due to a few divestments during FY2023 which include:

A 20% interest in associate in car-sharing platform GetGo Technologies Pte. Ltd. for S$7.9 million

50% interest in a JV of Amber 4042 Hotel Pte. Ltd. for S$23.3 million

05% controlling interests in LHN Logistics Limited for S$31.9 million

These capital recycling initiatives helped to shore up its financial position while funding the growth of its Coliwoo business.

5. Higher Dividends to boot

Notwithstanding the reduced profit attributable to equity holders, LHN has recommended a special dividend and final dividend of 1.0 Singapore cent each per share.

If we were to include the earlier interim dividend of 1.0 Singapore cent per share, the total dividend per share for FY2023 stands at 3.0 Singapore cents per share.

Based on the closing share price of $0.34 as of 26 November 2023, the dividend yield comes up to an enticing 8.8%, much higher than the estimated 3.5% yield of the STI ETF.

Looking at the dividends chart, LHN has been dishing out dividends consistently since FY2020. This shows the commitment of the management to continue rewarding shareholders – note that the management team happens to be the the Group’s biggest shareholder as well.

6. Management Team

From the table above, we can see that LHN Capital is the largest shareholder of the firm with a 54% interest. The holding company LHN Capital is in turn owned by the Lim family – Mr. Kelvin Lim and his sibling Ms. Jess Lim.

Mr. Kelvin Lim has been the Executive Chairman & Group Managing Director since July 2014 and possesses over 20 years of experience in the property leasing business, including over 10 years of experience in the logistics services and facilities management business.

Ms. Jess Lim, Executive Director & Group Deputy Managing Director, has over 20 years of extensive and varied experience in business and supply chain management, comprising of over 15 years of experience in the leasing and facilities management business.

Given that both of them own more than half the company, this aligns the interest of owner-management with minority shareholders.

7. Bright Outlook Ahead

In general, LHN expects a bright outlook for the company as its biggest segment stands to benefit from the rising demand for space optimisation solutions, as more people and businesses seek flexible and affordable space options.

Notably, the firm is gunning for substantial growth in the Coliwoo Co-living business as the ongoing renovation of properties at 404 Pasir Panjang Road, 48 and 50 Arab Street, and 99 Rangoon Road are on track for completion in FY2024. These developments are projected to contribute an estimated 121 keys to the Co-living portfolio.

Last but not least, the shift of its listing to the SGX Mainboard will bolster the Company’s standing both domestically and internationally, fostering greater visibility and recognition in the market and among investors.

Some industry background on the dynamics of Singapore’s co-living sector – for your consideration

Uni-Asia Group Limited is an alternative investment group specialising in creating alternative investment opportunities and providing integrated services relating to such investments.

The Group’s alternative investment targets are mainly Handysized Dry Bulk Cargo Ships and Property Investment.

Business Model

Their business model revolves around acquiring assets at competitive prices and offering solutions that meet client needs. After which, the company will operate and/or manage these assets to improve their value and boost the recurring income.

Maritime and Property Key Businesses

With that in mind, its easy to see why Uni-Asia focuses its portfolio on maritime and property investments.

A quick look at their asset allocation shows that their maritime investments contribute a major 60.5% of their portfolio as at 30 September 2023 whereas their property investments account for another 24.2%.

In the maritime sector, the Group maintains a fleet of 9 fully-owned and 7 jointly-owned dry bulk carriers, ensuring a consistent and reliable source of income through operational cash flows.

Their ongoing approach involves securing a blend of short-term and long-term charter agreements at varying rates, with the objective of optimising charter earnings during market upswings and fortifying against potential downturns.

In the latest earnings report, the Group has successfully concluded the sale of its oldest ship, M/V Uni Auc One, on November 10, 2023. It is noteworthy that the ship was free of any attached mortgage at the time of the sale, and all proceeds from the disposal have been seamlessly integrated into the Group’s cash balance.

As for the property segment, the Group invests in Hong Kong and Japan property projects.

In the first 3 HK projects, Uni-Asia had recovered capital and received/recorded strong positive returns in the past (i.e. HTR35, CSW650, and K83 in the picture above).

With economic activity in Hong Kong and China picking up post-Covid, it will provide a significant opportunity for the Group to generate substantial revenue by divesting its Hong Kong projects.

As for Japan, the Group typically invests and develops small residential property projects branded as the “ALERO” Series. This “ALERO” reputation has been established because every ALERO project that the Group invested in had been profitable since the Group started this series in 2011.

Stable Financial Position

Despite being in a high capex industry (shipping and properties), the Group’s total borrowings has declined steadily over the past few years due to scheduled repayment and prepayment of existing borrowings.

If you take a look at the chart above, Uni-Asia possesses a strong financial position with the debt/equity ratio coming in below 0.5x as of 1H2023.

Consistent Dividends

Uni-Asia Group has been delivering dividends to shareholders on a consistent basis since 2012. The Group’s gross dividends per share grew from 0.6 Singapore cents per share in FY2014 to 9.5 cents per share in FY2022.

The Group also dished out 2 cents and 5 cents in special dividends for the year 2021 and 2022 respectively, underpinned by the higher charter rates post-pandemic.

Taking into account the 5 cents in special dividends in FY2022, the total dividends per share would have exhibited a staggering 48% CAGR over the 8-year period from FY2014 to FY2022.

Last but not least, the Group has US$27.9 million cash on hand and generated operating cash flows of US$9.8 million for 9M2023. This is more than enough to pay out a decent 5 cents dividend per share amounting to an approximate US$4 million, and continue its debt reduction exercise in the long run.

Leadership Renewal

In the context of succession planning and leadership renewal, Executive Director Mr. Masahiro Iwabuchi will take on the role of Chief Executive Officer (CEO), succeeding Mr. Kenji Fukuyado. This transition will take place upon Mr. Fukuyado’s retirement on February 29, 2024.

The top 2 shareholders – YAMASA Co., Ltd and Evergreen International – are both in the property investment space, and own a 30% and 8.95% stake respectively in Uni-Asia. The similar nature of their businesses will harmonise effectively with Uni-Asia’s ongoing operations.

In addition, we can see that Chairman Michio Tanamoto and CEO Kenji Fukuyado both own a decent interest in the company. Incoming CEO Iwabuchi has also increased his stake in the firm by 7.63%.

Undemanding Valuation

Uni-Asia’s value is underpinned by its book value of ~S$2.30 per share as of 30 September 2023. At the time of writing, the firm’s share price is trading at roughly S$0.925/share, translating into an attractive 0.4x P/B ratio, significantly below the industry average of 0.9x.

It is worth highlighting that a significant portion of its balance sheet is supported by tangible assets, primarily consisting of property, plant, and equipment (mainly comprising the Group’s shipping vessels), along with investments, investment properties, and cash.

On top of that, this article points out that prices for bulk carriers have remained high, despite the declining trend in the dry bulk market. Increased newbuilding expenses, inflation, and substantial cashflows from high ship chartering rates have resulted in owners’ reluctance to sell vessels at reduced prices, and have led to buoyant second-hand prices in the market.

Hence, Uni-Asia may be able to lock in the positive gains by divesting its smaller vessels going forward.

Conclusion

In a nutshell, Uni-Asia remains a dividend favourite due to its focus on maritime and property investments, which will churn out recurring cashflows. An undemanding 0.4x P/B valuation also positions it as an attractive choice for investors seeking both capital and dividend returns in the realm of alternative investments.

The global Oil and Gas (O&G) industry has witnessed significant ups and downs in recent years. From the rise of renewable energy to the unrelenting impact of geopolitical tensions, the industry landscape is in a state of constant flux.

As we delve into the year 2023, it’s imperative to review the pivotal developments that have shaped the O&G sector and explore the implications for investors and stakeholders.

Shakeup in the Oil and Gas Industry

The O&G industry remains susceptible to market volatility, driven by factors such as supply disruptions caused by the COVID-19 pandemic and subsequent geopolitical tensions that resulted in huge price swings.

For instance, the West Texas Intermediate (WTI) crude oil futures’ price plummeted to a negative value for the first time on April 2020 as the COVID-19 pandemic spurred lockdowns all over the world.

However, the Russia-Ukraine conflict and subsequent events led to a rapid rebound in WTI crude oil futures’ price which hit a peak of US$139.13 per barrel on March 2022, the highest price since July 2008.

On top of that, the outbreak of the Israel-Hamas war has sent tremors through oil markets and stopped a decline in the oil prices triggered by a slowdown in the global economy.

The World Bank predicts that oil prices could skyrocket to a record high of US$150 if the ongoing conflict escalated into a scenario like that of the Arab oil embargo in 1973.

Although nobody can pre-determine the state of the O&G industry, market analysts expect oil and gas prices to remain elevated at current levels for the rest of the year and into 2024 at the time of writing this article.

3 O&G Stocks to Benefit

With that in mind, let’s take a quick look at 3 Singapore-listed stocks that stand to benefit in the tight global oil market.

1. Sinostar Pec

Sinostar Pec is a leading provider of services and solutions to the petrochemical and chemical industries in China. The key products of the company are Processed LPG, Propylene, Purified Isobutylene, Hydrogen, Methyl Tert-butyl Ether (MTBE), Polypropylene and Logistics and Transport.

For the 9 months ended September 2023, the Group delivered a decent 8.5% y-o-y growth in revenue to RMB3.77 billion.

On a brighter note, it recorded a net profit of RMB282.99 million in 9M2023, an increase of 313% compared to RMB68.51 million in 9M2022, underpinned by higher output and lower raw material costs.

The management remains upbeat on the stock’s prospects and commented:

“The Group’s business is driven by global economic recovery, demand growth, and rising crude oil prices. Barring unforeseen circumstances, the Group expects supply-demand dynamics to continue to improve. The board of directors remains optimistic about the Group’s long-term development.”

Based on a share price of S$0.15, Sinostar PEC trades at a modest 0.4x Price-to-Book ratio.

2. Dyna-Mac

Dyna-Mac is an offshore solutions provider, offering services to the oil and gas, marine, and petrochemical industries. The company is involved in the fabrication of topside modules for floating production storage and offloading (FPSO) vessels.

It provides engineering, fabrication, and construction of offshore FPSO and FSO (floating storage offloading) topside modules as well as onshore plants and other sub-sea products for the oil and gas industries.

For the 6 months ended June 2023, the Group reported revenue of S$182.3 million, up 47.0% compared to the previous year.

Net profit came in line, jumping over 200% from S$3.2 million in 1H2022 to S$10.2 million in 1H2023, attributable to better utilisation of capacity by intensifying land use, improved productivity and tighter cost controls.

On top of that, the firm has been securing new contracts aggressively, expanding its order book to S$630.7 million, with project delivery stretching into 2025.

The increase in orderbook is in line with the expected 8.0% CAGR growth of the FPSO market from US$11.91 billion in 2021 US$21.83 billion by 2028. This is being driven by significant demand in nations like Brazil, Mexico and Guyana, as well as exploration hotspots like Namibia’s Orange Basin and the East Mediterranean.

Drydocks World CEO Rado Antolovic has said he sees a strong pipeline for FPSOs and FSRUs for the next 5 to 10 years as the market pays more attention to offshore exploration and production operations, as well as rising deep- and ultra-deepwater exploration.

On this note, Dyna-Mac remains encouraged by the strong level of inquiries received for projects in both Singapore and China, indicating promising opportunities on the horizon. Dyna-Mac last closed at S$0.295, translating into a 15x P/E ratio.

3. Seatrium

Seatrium (formerly known as Sembcorp Marine) is a leading global marine and offshore engineering group with a track record of about 60 years. The company specialises in ship repair, shipbuilding, ship conversion, rig building, and offshore engineering and construction.

As seen from the picture above, Seatrium has achieved many commendable feats, such as delivering Singapore’s 1st LNG Bunkering Vessel and the World’s 1st Zero Emissions Ferry.

A buoyant O&G industry has also bolstered Seatrium’s orderbook – currently standing at a strong S$17.7 billion, comprising 33 projects with delivery schedules up to 2030.

Supported by a robust order backlog, the company’s revenue for 1H2023 jumped 160% to S$2.9 billion from a year ago, recording a notable increase of 164% from same period last year. It also registered positive EBITDA (before provision for contracts & merger expenses) of S$258 million for the same period, compared to negative EBITDA of S$19 million in 1H2022.

It is noteworthy that Seatrium has improved on its sprawling debt with net gearing coming in 0.17x as at 1H2023 vs 0.26x as at end Dec 2022.

Given that Seatrium is still reporting losses, we will take the valuation from a P/B point of view. Seatrium last traded at S$0.109 with a 0.9x P/B ratio.

Conclusion

While the world continues to grapple with heightened geopolitical tensions like the Russia-Ukraine conflict and Israel-Hamas war, higher oil prices will give a boost to the overall Oil & Gas sector.

Hence, the 3 stocks mentioned above: Sinostar Pec, Dyna-Mac, and Seatrium are likely to enjoy better margins and ride on the tailwinds of this O&G upcycle even as the industry adapts to the evolving energy landscape.

As someone who has lived through the Covid-19 period, one thing I would never leave home without is the TraceTogether token.

This has greatly benefitted the home-grown manufacturer of the TraceTogether Token – iWOW Technology. Its revenue jumped from S$4.4 million in FY2020 to FY2021 in FY2021 when Singapore adopted this technology islandwide.

But the question here is: what will happen to iWOW now that the TraceTogether Token has been phased out after the pandemic?

In this article, we will dive into how iWOW continues to ride on the Internet of Things (IoT) wave and expand its solutions to bag contracts worth S$100.4 million as of 31 October 2023.

One-Stop IoT Shop

To better understand iWOW, we take a closer look at their 2 main business segments and the types of solutions they provide.

As you can see from the picture above, revenue from the TraceTogether Token is delivered on a project basis. On the other hand, iWOW’s higher-margin IoT-as-a-Service segment provides high earnings visibility given its recurring subscription model.

Point to note: iWOW has developed this electronic monitoring system (EMS) which supplies ankle bracelets to young offenders and prisoners to monitor their whereabouts, and this contract provides sale visibility till 2027 (with the option to extend 2 years).

Tapping on the Expanding IoT market

Internet of Things (IoT) has emerged as a pivotal technology in the 21st century. The ability to connect everyday objects such as security cameras, kitchen appliances, doors, and thermostats to the internet through embedded devices has enabled seamless communication among people, processes, and things.

As per data from marketsandmarkets.com, the global Internet of Things (IoT) market is anticipated to expand from USD 300.3 billion in 2021 to USD 650.5 billion by 2026, demonstrating a Compound Annual Growth Rate (CAGR) of 16.7% from 2021 to 2026.

Within the local landscape, the Internet of Things (IoT) connections in Singapore have grown to approximately 63 million, surpassing the previous year’s figure of around 54 million connections. According to Statista, it is projected that the number of IoT connections will persist in its upward trajectory, reaching an estimated 143 million by the year 2028.

According to the Economic Development Board, Singapore has actively championed the widespread adoption of IoT by continuously upgrading its IT infrastructure, data collection & analytics.

One particular area where Singapore is looking to harness the power of IoT is in its road transport ecosystem. For example, Singapore is set to launch its next-generation electronic road pricing (ERP) system, utilizing IoT to monitor and oversee traffic conditions across the entire island.

You can also read more here: https://www.todayonline.com/singapore/better-living-conditions-seniors-emergency-buttons-rental-flats-2306471

As Singapore moves towards the development of a Smart Nation, it bodes well for iWOW Technology given its strong foothold in the city-state. The Group’s entry into IoT growth markets in Asia and the Middle East, such as Japan, Thailand, Malaysia, Indonesia and UAE, will provide yet another growth impetus. In fact, iWOW has registered a 181% CAGR in revenue between FY2020 to FY2022 by tapping on its solid track record and the tailwinds of fast-growing IoT adoption globally.

Stable Topline for 1H2024

iWOW’s revenue for 1H2024 inched up 1.2% to S$17.3 million as compared to S$17.1 million in the previous year.

Notably, this growth was achieved despite a 96.8% y-o-y decline in revenue from its Smart City Solutions segment, primarily due to the absence of TraceTogether Tokens sales and a delay in tenders for expected projects.

On a brighter note, the drop in revenue is mitigated by strong revenue contribution from the Smart City Infrastructure (“SCI”) segment with a top-line contribution of S$12.2 million in 1H2024 (versus “zero” in 1H2023).

Despite a stable 1H2024 topline, the Group witnessed an 88.2% Y-o-Y decline in net profit to S$0.3 million, largely due to a shift in product mix and higher costs from increased headcount. The latter will reinforce the Group’s R&D and business development capabilities to capture near-term growth opportunities and accelerate project completion.

Confident of 2H2024 with Record High Order Book

iWOW Technology’s order book experienced a nearly twofold increase, rising from S$54.4 million as of 30 September 2022 to S$100.4 million as of 31 October 2023. Consequently, the Group is cautiously optimistic about its revenue performance for the second half-year ending 31 March 2024 (“2H2024”).

In particular, the Group foresees a jump in revenue in 2H2024, led by its Smart City Infrastructure segment as it fulfills the majority of installation tasks for an estimated S$20.0 million contract announced on July 21, 2023 – inclusive of 10 years of recurring maintenance services.

The Group believes that the steadfast focus on expanding the Group’s higher-margin subscription-based business will allow iWOW to benefit from improving future earnings visibility.

Mr. Raymond Bo, Chief Executive Officer and Executive Director of iWOW Technology, remains sanguine about the company’s prospects:

“We have been strategically boosting our R&D investment to strengthen our position and enhance our ability to capitalise on potential opportunities. We are also constantly leveraging on our network and strategic partners in our pursuit of regional opportunities.”

High Insider Ownership

Based on the ownership table above, it indicates that management interests are well aligned with that of retail shareholders. For instance, Mr Kee Wee Soo, Chairman of iWOW Technology Limited, owns a sizable 46.59%.

If you move down the list of top shareholders, you can see that they are also part of the management team. Even Mr. Ashokan Ramakrishnan, the Head of Marketing, owns a good 2.8% interest worth S$1.6 million.

This strong alignment of interests can potentially retain key employees and encourage executives to make decisions that are in the best long-term interests of the company and its shareholders.

Conclusion

In conclusion, iWOW Technology has established a solid track record and become a trusted IoT solution provider for Singapore government agencies and B2B customers such as Singtel, 3M and Mapletree over the years.

As evident from its increase in its order book, especially in the Smart City Infrastructure segment, iWOW’s revenue is not solely supported by the success of the TraceTogether Tokens, but by a wide array of solutions.

Moving forward, iWOW is well-positioned to ride the IoT wave with further investments in its R&D capabilities to develop new wireless technologies i.e. LoRaWAN, 5G and NBIOT.

My Cart 0

My Cart 0