My Cart 0

My Cart 0

GEM COMM: Alliance Healthcare (MIJ) announced FY2020 net profit attributable to shareholders increased to S$2.3 million on revenue of S$42.8 million

- Declares first and final dividend of 0.34 Singapore cent, representing pay-out ratio of 30%

- New mobile and digital health services segment recorded maiden revenue contribution

- Pivot to digital interface to meet growing demand for virtual healthcare services

Click here for the press release

Exerpt from Smallcap Asia

![]()

Ever since the virus outbreak started since the beginning of 2020, Singapore has undergone a ‘lock-down’ period with all large-scale concerts/events postponed or cancelled until further notice.

The adverse impact has been especially so for UnUsUaL Entertainment (“UnUsUaL” in short) with concerts around Asia literally come to a standstill. Hence, it’s of no surprise that its shares have been hammered from around S$0.30 in December 2019 to S$0.14 as of around 20 August 2020.

Is the worst over for UnUsUaL given the gradual opening up of the economy? Does UnUsUaL shares contain hidden value waiting to be unlocked?

To try to answer the questions, we take a deep dive into its business model and catalysts below to find out more. But first, here’s a quick background of UnUsUaL.

UnUsUaL Limited Profile

UnUsUaL Limited operates as a production and promotion service provider for events and concerts. The Company provides services in staging, Sound Light and Visual (SLV) for an event and a concert, and organize and promote concerts.

With a track record of over 20 years, it has grown to be one of the leading names in Asia, specialising in the production and promotion of largescale live events and concerts by Asian and International artistes.

As a Promoter, UnUsUaL will liaise with artiste managers to bid for the right to host various concerts or shows in each relevant city. After a successful bidding, the Group will take charge of planning, managing and marketing of the event.

As a Production Company, UnUsUaL will provide overall support to concert or event organisers in their set-up and installation, including stage creation and design. With one of the largest technical equipment inventories in Singapore, UnUsUaL is frequently involved in large scale events such the 28th SEA Games Carnival and the Singapore Grand Prix.

3 Key Highlights Investors Should Know

Below, we will go through some of the key things investors should know about the company before one can ascertain if there’s any hidden value to be unlocked in UnUsUaL.

1) FY2020 Results ended 31 March 2020

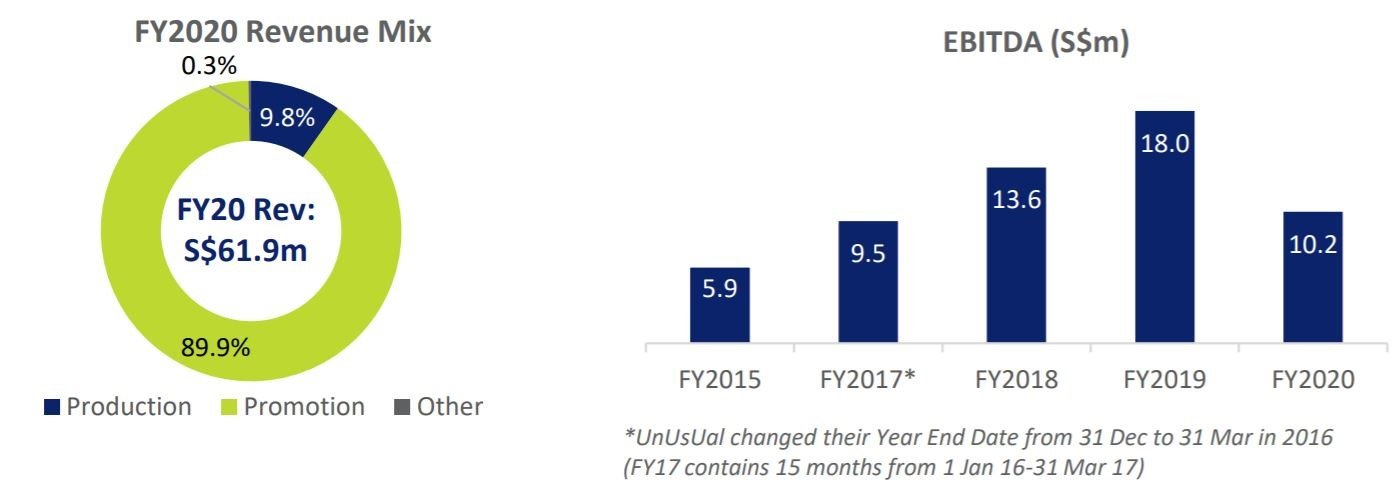

UnUsUaL announced its FY2020 results on 27 May 2020 and saw net profits shrink 52.3% to S$6.3 million because most of the concerts and events in 4Q FY2020 have been postponed.

CEO Mr Leslie Ong remain steadfast in the face of uncertainty and commented (edited for context):

“We are dealing with an unprecedented and fluid situation. However, the good news is that the company’s financial position and liquidity remain strong.

We believe our efficient business model and the recent steps we have taken to strengthen our balance sheet leave us well-positioned to navigate and manage our business through this crisis.

Our strong relationships with established artistes and their managers has allowed us to maintain our existing pipeline of events. We remain cautiously optimistic of the Group’s long-term business prospects”.

2) UnUsUaL’s Revenue Mix

UnUsUaL’s revenue comes from 3 main business segments:

- Promotion revenue is derived from total sales generated from a concert/show less the cost of hosting the concert/show. This segment is the largest contributor to our revenue base.

- Production revenue is derived from provision of technical and creative expertise to large-scale live events/concerts.

- Other revenue is derived from rental of exhibition/concert halls and related equipment and comanagement of exhibition/concert.

According to UnUsUaL’s interview with SGX 10 in 10 series, while promotion and production segments will continue to be major contributors to the group’s profitability, they may explore other businesses opportunities such as e-sports or sales of event tickets too.

According to UnUsUaL’s interview with SGX 10 in 10 series, while promotion and production segments will continue to be major contributors to the group’s profitability, they may explore other businesses opportunities such as e-sports or sales of event tickets too.

But for the near term, investors should not be surprised if UnUsUaL reports losses for FY2021 due to the postponement of major concerts and events.

3) How UnUsUaL is handling Covid-19

As previously mentioned, UnUsUaL is adversely impacted due to its nature of the business. To navigate these unprecedented times, the firm has taken steps to strengthen its balance sheet including:

- Reduction in payroll (with the support of its staff)

- Immediate cuts in discretionary expenses and

- Negotiating for revised payment terms on existing commitments.

Taking an excerpt from KGI analyst report, UnUsUaL has enough cash of S$12.6mn at end-March 2020 to tide them across the next 3 years.

This is done by a back-of-the-envelope calculation where employee expenses will fall 30% to S$2.3mn and other expenses of S$1.5mn will bring total cash expenses of S$3.8mn per year.

All other expenses such as manpower/subcontractor (S$5.3mn in FY2020) and transportation/freight costs (S$2.0mn in FY2020) are highly dependent on whether it can organise such large-scale events. As a result, these will not be a drag on its cash flows in FY2021.

Impending Catalysts: Is UnUsUaL Undervalued?

Now that we know that UnUsUaL will probably go through a year of underperformance due to the pandemic but has enough cash coffers to tide them through, the next question would be whether there are catalysts to bring UnUsUaL out of the woods.

With that, we actually see a couple of silver linings which others may have missed out amid this gloomy situation…

1) Negatives may be Priced In

Sourced from ShareInvestor.com

Sourced from ShareInvestor.com

If you look at the share price chart above, the stock’s volume have practically dried up after April 2020. In addition, the stock price and 20-ma and 50-ma lines are all congesting together around the S$0.13 to S$0.15 region.

This shows that the stock is in a consolidation phase with limited selling pressure. In other words, it seems like the negatives have been priced in by the investors and any good news may propel the share price upwards.

2) Shows already running + Shift to Online

In case you aren’t aware, live concerts are already ongoing in Taiwan. Check out the link here and here. However, according to KGI analyst report, although both shows ran at 100% physical capacity (i.e. 10k seats), UnUsUaL only managed to secure about a 30% cut as they were unable to be there physically and had to outsource the management and production of the shows, due to travel restrictions.

That said, it is a positive sign that countries that Covid-19 is under control are slowly opening up for concerts/events again.

On the other spectrum, online live-streaming of live concerts could become the new norm in future as the Covid-19 recovery remains a big question mark to UnUsUaL’s core business.

In fact, investors can find a silver lining from South Korea’s BTS’s live concert ‘Bang Bang Con’. Check out this live reaction from a viewer attending it online. Based on Straits Times’ article, the online concert welcomed 756,000 viewers at its peak and raked in an estimated S$26 million based on selling price of S$35 (1/5 of usual ticket price).

The management team also expressed their intention to head towards this direction:

“During this period, we have also noticed a rising demand for virtual concerts. The Group is currently working on digital distribution and live streaming of these shows. We are looking to gradually roll out concerts in 3Q FY2021 in markets which have resumed economic activities.”

3) Potential Buyout by much Larger Peers

If you have done some research, you would be aware of this live concert company based in U.S. called Live Nation Entertainment. It actually expanded to Taiwan and Singapore in Feb 2020 via its subsidiary called Ticketmaster. You can find out more about their expansion here and here.

Trading at S$0.135, UnUsUaL’s market capitalization stands at a mere S$138.9 million. This is in stark contrast to its peers like Live Nation Entertainment which boasts a US$11.2 billion.

During such a depressed period where no one knows when the crisis will end, there may be a chance that Live Nation may choose to undertake an acquisition of smaller peer – UnUsUaL Entertainment.

Conclusion

To conclude, UnUsUaL has an asset-light and relationship-based business model. This allows the firm to be in a good position to swerve through this prolonged crisis.

Although it may take a long time to stage a full recovery with the ongoing pandemic, the pent-up demand and pivot to online concerts may help UnUsUaL emerge even stronger than before.

Links for Reference

https://www.businesstimes.com.sg/companies-markets/unusual-keeps-faith-in-live-events

https://www.gem-comm.com/old-backup/our_research/unusual/

Earnings of Alliance Healthcare surged 635.1% to $2.3 million in FY2020 ended June 30, from the $0.3 million posted a year ago. The latest full-year results is a first for the company which went public at 20.5 cents a share on May 31 2019.

On a fully diluted basis, this translates to earnings per share of $1.12 in FY2020 compared to 15 cents in the previous year end.

The improved performance follows a 17.2% increase in its revenue to $42.8 million in FY2020, thanks to higher income from its pharmaceutical services segment which benefitted from hospitals’ stock piling of medical supplies to meet demand and in preparation of supply chain disruptions.

The maiden contribution from its mobile and digital health services aided in lifting its income.

THE EDGE, 28 Aug 2020

Click here to read more

Eagle Hospitality Trust Sponsor Urges Collaboration to Save REIT

- Urban Commons believes it is time to unite and deliver a sustainable survival plan for the REIT

- The Sponsor objects to deliberately being portrayed in a negative light

GEM COMM SINGAPORE, August 21, 2020 – In a Breach Notice sent to Eagle Hospitality Trust (EHT or REIT), Urban Commons (UC or Sponsor or Master Lessee), the Los Angeles-based real estate investment and development firm and Sponsor of EHT, has strongly objected to the continuous negative aspersions being levelled against it by EHT. UC believes that its reputation is being deliberately damaged at the behest of EHT’s advisors and this is against the best interests of the ordinary unitholders of the Trust as the focus should be about the survival of the business.

An ageing population and rising healthcare costs are long-term trends that Alliance Healthcare is zeroing in on as it expands its managed healthcare services business, executive chairman and CEO Barry Thng told The Business Times.

The Catalist-listed firm in January took a 55 per cent stake in home-based care startup Jaga-Me for S$3.5 million, and in May rolled out a digital health platform for corporate clients aimed at making healthcare more accessible.

Through its investment in Jaga-Me, Alliance now wants to expand its managed healthcare business further by bringing care directly to the doorsteps of patients, including the elderly. Jaga-Me’s smartphone platform connects over 500 licensed healthcare professionals to people who have chronic diseases or require post-hospitalisation care.

Alliance and Jaga-Me are working on some pilot projects with insurers to test aspects such as cost-efficiency and customer experience.

One of the cases Jaga-Me handled involved a 68-year-old female who suffered a haemorrhagic stroke and was bed-bound. Her stay in a private hospital cost an average of S$1,500 a day, translating to S$45,000 a month.

The patient was eventually moved to home-based care. Jaga-Me created a personalised care plan that included home-nursing procedures, medical care, caregiver training and home physiotherapy. Together with a domestic helper hired for assistance, the monthly cost came up to S$9,500.

BUSINESS TIMES, 3 AUG 2020

Click here to read more