Like any typical Asian household, money was rarely discussed at home. That kept me blissfully oblivious to the perils of money making in my teen years, but led me straight to a few painful (and expensive) lessons in my early 20s.

The unfortunate thing is that these lessons are in no way isolated to the early 20s of our lives. If left unchecked, one could repeat these mistakes all throughout life. And that’s not because we’re not smart enough to handle our finances, but because money isn’t just numbers on a sheet, but oftentimes tied to our habits, beliefs and emotions. Because if it were just numbers on a sheet, most of us should be able to work out how to save and spend quite easily.

Every investment seminar will tell you not to invest with your emotions. Same principle applies to everyday finances.

Avoiding these common money pitfalls will require some harsh truths to be heard. Starting with…

Not confronting the truth about your finances

Money is usually a very confronting topic simply because it causes discomfort and inconvenience.

Want to buy a better work from home chair to ease your back pains? But wait…ergonomic chairs cost $300, that can go to paying my student loan… Going out for a nice dinner with friends? Wait a second…how are my ex-classmates able to afford this expensive restaurant?! This takes a huge chunk out of my budget!

Not being able to get what we want is hard to deal with. You’d think that as mature adults we would be able to delay some gratification to fulfil more important responsibilities first. However, and quite unfortunately, just like children crying for candy, adults have their own form of candy that they simply can’t resist. Only this time no one will tell us that we can’t have it. On the contrary, we have plenty of sales people pestering us to spend (more).

This candy is sweetener for the painful, embarassing, disappointing state of our finances. I’ve been in that place of denial – not wanting to confront exactly how much debt I’m in, and just hoping to live (read: spend money) blissfully ignorant of the truth. Nothing good comes out of that except more debts piling up, and less cash resources to deal with it.

So before you act out of impulse just to bury away the pain of your actual financial situation, put aside your emotions and take time to take stock of your current resources. How much savings do you have? How much debt are you in? There’s no shame if it comes down to a negative number. The more important thing is to have a good look at that, and start devising a plan to improve your financial health.

Spending money to impress others

The work from home life has opened our eyes up to how little we really need to work. Fancy office locations aside, many of us also needed to keep up with appearances at the office, spending hundreds of dollars monthly on clothes, cosmetics and more.

Some people spend money they don’t have on luxury cars to impress their friends. Others spend on luxury handbags to stay in the good books of their office clique.

The question to consider is this: what would you cut out from your expenses if you didn’t have to impress anyone?

It’s okay to splurge on big ticket items, but only if you can realistically afford the item and it serves you well. Otherwise, your hard earned money in your early 20s can be better channeled towards something like a savings fund.

Not saving for an emergency fund

Yes, not saving for an emergency fund is one of the biggest mistakes anyone can make.

You can feel like you’re invincible when you’re 20. Your health is in tip top condition, and you won’t be the unlucky one to meet with an accident.

But I’m pretty sure Covid-19 has cleared any misguided perceptions we might have about our invincibility. In truth, none of us are immune to the uncertainties of life. While we’re not going about life waiting for the worst to happen, an emergency fund does provide a peace of mind to let you know that you have something to fall back on.

There are a few milestones to aim for, so it doesn’t feel so overwhemling to save a large amount at one go. You can start by saving up 6 months of expenses, then progressing to 6 months of your salary. A solid savings account is also a must have before you start investing, which should provide a little motivation to get this done fast.

Underestimating your value

Many fresh grads often fall into the trap of underestimating their value in a company, opting to accept a lower salary thinking it’s fair for their lack of experience. Experience is important, but there are a few soft skills that can give you some additional brownie points. A good attitude, a willingness to participate and even being street smart are some soft skills that can help you excel in the corporate world.

We’re not saying you should ask for a manager’s salary, but please go into any interview with a clear idea of the value you provide. Here are a few questions to consider:

- What is the value (hard skills, soft skills) I can provide to the company?

- How much work is the company expecting me to do?

- What is the career progression like in the company and in the industry?

- Does this job fulfil my interests and passion as a person?

The definition of a good and fulfilling job differs from person to person. Instead of listening to generic advice like “money is not everything” or “follow your passion”, it’s more helpful if you can determine your own set of factors that are important to you in a career. These factors should directly compensate you for the time and effort you will be giving away.

Not all factors need to be money related. It’s good to be more strategic about your career so you can plan your way into a career path that reflects your value as an individual. Things like a good exposure to diverse clients, working with an experienced industry player, or a company that aligns with your personal values are some factors that if met, can provide that much needed purpose and motivation for daily work.

Not planning ahead

I made the mistake of diving head first into my first career without researching more into the career prospects and progression for my industry, and this directly affected salary, savings, expenditure, the lot.

The corporate world tends to pigeon hole people very quickly. Unless you’re very sure of the industry you want to be in, think twice before you commit to any particular specialisation.

Try to speak to relatives or seniors to understand the corporate landscape better. They don’t have to be in the industry you’re interested in. Speak to them to find out more about the recruitment process, career prospects, how to climb the corporate ladder and how to exit the corporate race in future.

Plan meticulously, it really doesn’t hurt to research more before you jump into anything.

Hopefully these tips are useful to you. Do let us know in the comments what you want to hear from us in future!

About GEM COMM

We are an International Investor Relations firm (IR) based in Singapore. We specialise in Investor Relations, Public Relations, marketing, branding and messaging strategies for clients that include organisations of all sizes across Asia, Oceania and US.

GEM COMM advice and solves stakeholders’ issues, drive growth, reposition your business, improve your marketing and Public Relations (PR) or engage with investment community in your leadership or strategy story. We have a track record of helping clients reach these goals. We create and implement PR & media content, mitigate crisis and issues, establish and improve thought leadership & content marketing.

GEM COMM Engagement types include:

– IR/PR retainer program

– Crisis and issues projects;

– Content marketing (from research to lead generation) inclusive of Press Release drafting, Media Pitch, Website content, etc.

See more on our factsheet.

Follow us on Telegram, Instagram, Facebook and LinkedIn for more finance tips coming your way!

As a first time investor, I’ve been researching about different investment strategies, starting with the ones that are beginner friendly.

Because I’m such a noob at all things finance, it was a really steep learning curve to understand what all the finance terms were, and then what each investment strategy meant (and this series is a place for me to share my findings).

You don’t know what you don’t know, so I spent weeks ploughing through countless blog articles, before finally deciding to put the studying on pause and shift gears into actual field study. Perhaps that will help me learn better.

One thing all first-time investors might want to consider is a regular savings account, especially if you have a small investment budget to begin with. You can look into DBS Invest Saver or OCBC Blue Chip Investment Plan.

Logging into my DBS iBanking account to check out their Invest Saver account, I hit my first road block.

What are equities and bonds?

Of course, I had not think to search that because it wasn’t really in my vocabulary.

I’ve heard of these terms, but a savvy investor should know their investment products well, right?

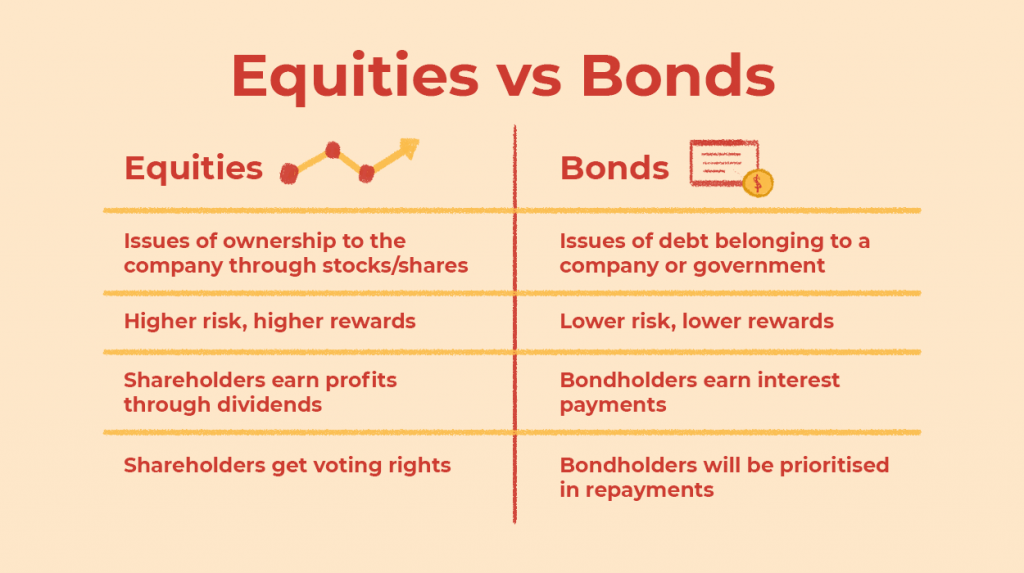

First things first, definitions. Equities refers to stocks or shares, which gives you a some ownership of the company when you buy them. Bonds on the other hand are the company or government’s debts, which you can purchase to receive an interest on the loan after a period of time.

Here’s a quick summary of what equities and bonds are.

Key differences between equities and bonds

Equities, or shares, typically are a riskier investment vehicle compared to bonds. Shareholders are not guaranteed any returns. Your investments are entirely based on your judgement of the company, and the company’s ability to make profits. Bonds are considered safer as bondholders will be repaid first in the event that the company does go belly-up. That said, higher risk higher rewards, and historically, stocks have performed better than bonds since 1928.

You do get paid regularly as a bondholder, depending on the type of interest repayment. What’s most attractive about bonds are the regular cash payments that bondholders receive. It’s an additional stream of predictable income that conservative investors can’t reject. On the other hand, you can only make money from shares when you sell it at a higher price on the market, which is dependent on a whole host of factors.

So which should I choose?

As with all investment strategies, balance is key. Your portfolio can contain a mix of equities, bonds, and other investment vehicles as well, which is probably the way to go.

The tricker question is how much money should be allocated to each type of investment. This is dependent on your risk appetite and invesment horizon. What are your investment goals? Are you building your reserves to make a big purchase down the road? Are you saving long term for retirement? Asking these questions will distill the options available into the ones most suitable for you.

Of course, you have investment strategies you’d like to share with this investment noob, do leave a comment below! And follow us for more invesment and finance news coming your way.