My Cart 0

My Cart 0

HC Surgical expands GP network with Medistar Services Pte. Ltd

- Onboarding of 3 veteran GPs with more than 40 years of experience in primary healthcare, and a stable pool of patients for referrals

- Expands GP network footprint to central Singapore, within close proximity to prime residential districts and private hospitals

Catalist-listed HC Surgical Specialists Limited (SGX:1B1) (“HCSS”, or collectively with its subsidiaries and associated companies, the “Group” or the “Company”) today announced that it has entered into a Sale and Purchase Agreement (“SPA”) with Dr. Tan Hooi Hwa (“Dr. Tan”), Dr. Pang Heng Mun Roger (“Dr. Pang”) and Dr. Wong Yik Mun (“Dr. Wong”) (collectively the “GPs” or “Vendors”), to acquire a total of 25.0% of the total issued and paid-up share capital of Medistar Services Pte. Ltd. (“Medistar”) for a total purchase consideration of S$480,000 (“Purchase Consideration”) (the “Proposed Acquisition”). Dr. Lai Junxu, a general practitioner with the Group, will acquire 5.0% of the total issued and paid-up share capital in Medistar.

The addition of the GPs will strengthen the Group’s capabilities and is in line with its plan for growth and expanding its presence in Singapore as HCSS’s team of GPs will increase from five to eight.

Chief Executive Officer of HCSS, Dr. Heah Sieu Min said: “The Proposed Acquisition of Medistar is in line with our strategy of business expansion by acquiring GPs to secure a consistent stream of patients through GP referrals. Dr. Tan, Dr. Pang and Dr. Wong are industry veterans with a stable pool of patients, and we are very excited for them to join our HCSS family. The strategic location of The Ming Clinic, which is in near proximity to Singapore’s prime residential districts and the neighborhood of private hospitals such as Gleneagles and Mount Elizabeth Hospital, will further expand our GP network to the heart of Singapore.”

MM2 ASIA: STRONG REVENUE GROWTH IN ALL BUSINESS SEGMENTS

- mm2’s FY2019 revenue rose 38.6% y-o-y to S$266.2 million on the back of full year contributions from its cinema business

- Company recorded a net profit of S$28.7 million in FY2019

- Company remains focused on enhancing consumer experience in regional markets, particularly through Out-of-Home Entertainment Platform businesses

mm2 Asia Ltd. (“mm2 Asia”, “mm2 全亚影视娱乐有限公司” or collectively with its subsidiaries, the “Group”), today announced its financial results for the full year ended 31 March 2019 (“FY2019”).

Chief Executive Officer of mm2 Asia, Mr. Chang Long Jong (章能容), commented on the Group’s results, “FY2019 performance was a collaborative effort delivered by the Group. We saw, for the first time, the full year contribution from our Singapore cinema operations, and the results are encouraging. On the other hand, our content production, post production, and event production and concert promotion businesses have all made inroads in North Asia. We continue to see operational synergies across our business segments, which we look to capitalize on going forward.”

Executive Chairman of mm2 Asia, Mr. Melvin Ang ( 洪伟才) , annotated, “Amidst the global economic uncertainties and heightened market risks, we remain optimistic in our pipeline of regional projects, which include a slate of feature films, concerts, and family entertainment shows. Simultaneously, we are looking to strengthen our value proposition as one of the leading content creators in Asia, with an increasing focus on our Out-of-Home Entertainment platforms, led by UnUsUaL, Vividthree and mm2 Asia’s cinema business, to collectively enhance our consumer experience across regional markets.”

Mr. Ang added, “Enhancing shareholder value has always been a key focus for us. We are actively exploring different avenues to maximise shareholder value, including the possibility of seeking a foreign listing of our cinema business.”

We provide free daily news update on the market and the economy on whatsapp and telegram.

To subscribe:

Join our telegram group: https://t.me/gemcomm

Join our whatsapp broadcast: txt hello to

https://api.whatsapp.com/send?phone=6587407951&text=&source=&data=

Service of: https://www.facebook.com/GEMCOMM.IR/

Pls let your friends know if you like our service. Thanks.

________________________________________________________

GEM Exclusive- Investment Idea-INNOTEK

INNOTEK Ltd.

Mkt cap: $118m; Price: $0.52, P/B: 0.77x, 2018 P/E: 5.8x, Ex-(cash+financial assets) 2018 PE: 2.4x; ~2-2.4x EV/EBITDA, Dividend yield: 2.9%

About: Precision metal components manufacturer serving mainly Office Automation, Automotive, TV & Display with over 40 years of operational history; Customers include major MNCs such as Ricoh, Canon, Continental, Sony, Innolux, Epson, Bosch, Innolux

Nearly 100% of Valuation backed by hard assets= Cash (S$0.257) + Investments (S$0.053) + Investment properties (S$0.120) + buildings and land only in PPE (S$0.07) = S$0.498

___________

Net cash of S$0.257/share as at 31 Mar 19 (after adjusting for S$0.01 dividend paid on 22 May 19)- forming about 50% of market cap-S$39.6m cash, S$20.7m in structured deposits (a combi of deposit and investment product, investors will receive 100% of principal if held till maturity). If you include the investment portfolio (equities, trusts, bonds etc) of S$12m, it will boost net cash + financial assets = S$0.310 (about 61% of mkt cap)

Strong Free cashflow generation- average S$0.043 of free cash generated/year in the last 3 FYs – notwithstanding any dividend payment and if innotek maintain its cashflow generation, it will take about 5 years for Innotek’s market cap to be fully backed by $.

Huge Turnaround attributable to savvy management- who came on board in late 2015, and the turnaround has almost been immediate, with Innotek successfully reversing from a loss in 2015 to a profit in 2016, before nearly doubling in profit (from 2016) to S$20m in 2018. It is always reassuring to see Management who are always adapting to market trends and not resting on their laurels, as in the case of Innotek – With good foresight, Management had diversified into heatsinks, automotive displays earlier on, which had helped to soften the impact of a declining trend where tradition metal TV bezels are being replaced by plastics. Similar can be said by management’s decision to set up a new facility in Thailand to be nearer to its customers (short term pain, long term gain), regaining market share for its office automation. Innotek is now looking to be an even more integral part of its customer’s supply chain as it transits from single component supply to assembly.

Management put his money where his mouth is. In 2016, Mr Lou (CEO) owns about 5.3% stake in innotek. He doubled his stake in the group in Jul 18 to 11.5% by acquiring shares in the group at S$0.40/share- tying his fate even more closely to shareholders.50% rise in dividends With the improvement in profit, Innotek has also rewarded shareholders with a 50% rise in dividends to S$0.015 for FY18, (a needle in its haystack of S$0.31 worth of $$)

Stellar 1QFY19 results with a 29% rise in gross profit, and a surge in net profit (amidst a low base) to S$3.9m. Free cashflow generated was super strong too (S$0.054/share). However, share price has fallen 15% since, on concerns of a weaker outlook from a slower Chinese economy and greater macro uncertainty.

What we think: While the outlook is more murky for cyclical stocks such as Innotek, its low valuation (one of the lowest among its peers, and also happened to be backed nearly 100% by hard assets (thinking from a liquidation perspective), gives Innotek a high margin of safety for investors. Investors can also sleep with a peace of mind that the company is currently run by a savvy management who have proven themselves over the last 3 years (including their ability to adapt to market trends) and also put his money where his mouth is, riding the up and downs with shareholders. With its cash flow generative nature, innotek will only get “cheaper” as time goes by as cash accumulates.

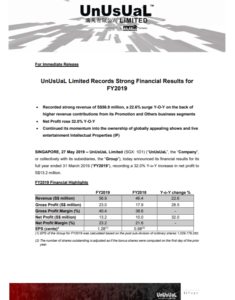

UnUsUaL Limited Records Strong Financial Results for

FY2019

- Recorded strong revenue of S$56.9 million, a 22.6% surge Y-O-Y on the back of higher revenue contributions from its Promotion and Others business segments

- Net Profit rose 32.0% Y-O-Y

- Continued its momentum into the ownership of globally appealing shows and live entertainment Intellectual Properties (IP)

UnUsUaL Limited (SGX: 1D1) (“UnUsUaL”, the “Company”, or collectively with its subsidiaries, the “Group”), today announced its financial results for its full year ended 31 March 2019 (“FY2019”), recording a 32.0% Y-o-Y increase in net profit to S$13.2 million.

The local and regional live entertainment industries remain competitive and challenging. In this regard, we have established our plans for the next 12 months, which include the Promotion and Production of globally appealing shows in addition to our usual offerings of concerts by well-known artistes. With this, we look towards a reasonable performance ahead.

Annotating on the Group’s FY2019 results, Chief Executive Officer of UnUsUaL, Mr Leslie Ong said, “It has been an exhilarating year with many critical opportunities that opened doors for us. Looking back at our achievement in the past one year, we are especially gratified with how far we have come today as a Group. The Group’s financial performance in FY2019 is a testament to our hard work and a reflective indication of our capabilities as one of the leading names in Asia in the industry. As we keep our momentum and chart further growth ahead, we will continue to improve operations and strengthen our business with better entertainment products that can excite and grow our audience and boost our target audience beyond the traditional concert goers.”

Vividthree Holdings Reports Positive Growth in 4Q2019

- Recorded 4Q2019 Revenue rose 121.6% y-o-y to S$4.0 million

- Net Profit surged more than twentyfold to S$1.5 million in 4Q2019

- Gross Profit margin jumped by 29.9% to 68.6% in 4Q2019 due to better margin yielded by its Content Production segment

- Train To Busan Virtual Reality (“TTB VR”) tour show extends to another province in China, Xiamen, with 1-year exclusive territorial rights granted to the local promoter

Vividthree Holdings Ltd. (SGX: OMK), a virtual reality, visual effects and computer-generated imagery production studio (“Vividthree”, the “Company” or the “Group”) today announced its financial results for its three months ended 31 March 2019 (“4Q2019”) and full year ended 31 March 2019 (“FY2019”).

Looking ahead, the Group remains focused on strengthening their presence in Asia as a digital content producer. Following the completion of its flagship TTB VR tour show in Beijing, the tour show will subsequently travel to another province in China, Xiamen, where the Group has engaged a local promoter by granting them a 1-year exclusive territorial rights to host the tour show in the particular province. The Group will also be tapping on the worldwide success of the Korean blockbuster, TTB, which will soon have a sequel slated for release in 2020. As a result, the Group has received warm responses from several promoters in the region, and it is currently in negotiations to take the TTB VR tour show to other parts of the world.

Managing Director of Vividthree, Mr Charles Yeo commented, “This set of results marked a good finale to the fiscal year 2019. We are just at the beginning, the tip of the iceberg. As we gained positive traction in our Content Production business, particularly the Train To Busan Virtual Reality tour show, we are proud to unravel it to more vibrant provinces in China, such as Xiamen while exploring more opportunities across the globe. We will keep up our continued momentum in actively seeking more evergreen intellectual property products and constantly aim to maximise shareholders’ returns in the longer term.”

Riding on the fast-growing experience economy, the Group is also looking into the use of VR technology to improve the experience of an escape game (a room filled with puzzles and scenario games), which has become a worldwide craze in recent years. The Group will continue to look for merger and acquisition opportunities, as well as new intellectual property products to expand its Post-Production and Content Production businesses.

SingPost & Synagie partner to provide on-demand

warehousing and logistics solutions for SMEs in

Singapore and Southeast Asia

- Synagie to collaborate with Singapore Post to provide cloud-based warehousing and fulfilment solutions

- Collaboration will enable small and medium-sized enterprises to utilise state-of-the art warehousing services in Singapore and Southeast Asia

Southeast Asia’s small and medium-sized enterprises (SMEs) will now be able to utilise stateof-the-art warehousing and fulfilment services provided by SingPost subsidiary Quantium Solutions, and powered by Synagie’s cloud commerce platform. The partnership will enable SMEs to capitalise on the strong growth in eCommerce order volumes while enjoying the same enterprise grade logistics capabilities used by industry leaders. It also offers SMEs a one-stop solution for greater operational efficiency and faster turnaround times in both the traditional and eCommerce markets.

SingPost’s partnership with Synagie to provide on-demand warehousing allows brands and SMEs to save on the heavy upfront capital expenditure required to set up or operate their own warehouse, as they are able to acquire integrated warehousing services on a pay-as-you-use basis without long-term commitments. This highly scalable solution will better help them cater to the spikes in warehousing demands during peak seasons (such as mega sales events) and provide greater cost savings and better inventory management.

Commenting on the partnership, Synagie’s Executive Director and CEO, Clement Lee said: “We are honoured to collaborate with SingPost to provide one of the region’s first fully integrated on-demand warehousing and fulfilment solution focused at helping SMEs manage their multi-channel supply chains. By combining our solutions and infrastructure, we can provide a fulfilment ecosystem for brands and SMEs that will bring about greater efficiencies and cost savings for both their offline and online businesses.”

SINOSTAR PEC 1Q2019 RESULT UPDATES

中星石化2019年第一季度净利润激增82%

- Revenue rose 85% Y-o-Y to RMB 979.5 million driven by maiden contributions from newly acquired subsidiary, Dongming Qianhai at end of FY2018

- 由于2018财年末新收购的子公司东明前海的贡献,

中星石化的收入同比增长85%,达到979.5百万元 - Net profit grew 82% Y-o-Y to RMB 38.8 million

- 净利润同比增长82%,达到38.8百万元

The Group’s propylene production plant at Dongming Qianhai has been in stable production since the start of FY2019, and began contributing to our group in the past quarter.

Polypropylene is the most important derivative of propylene and is calculated to form more than 70% of propylene demand. In tandem with our expanded propylene production capacity, the Group is constructing a new polypropylene plant and presently at the piling completion stage. The construction of the polypropylene production plant is estimated to complete by the third quarter of fiscal year 2020.

The Group will continue to focus on cost efficiency along with increasing frequency in cost budget review, and remain cautiously optimistic about its ability to achieve profitability in 2019.

Mr Zheng Liucheng, Chief Executive Officer and Executive Director of Sinostar PEC, commented, “We are really pleased with our 1Q2019 results. With the consolidation of Dongming Qianhai, we have beefed up our production capability and expertise to produce more value-added products such as MTBE and Isobutylene. We will continue to execute on our expansion plans while being mindful of our cash flow and gearing to maximize shareholder value”

Download Press Release (Chi) Sinostar_PR_1Q19 chi version-1

Synagie Signs New Brand Partner with Luggage Giant,

Samsonite

- Manage the online sales of Samsonite, Samsonite Red, American Tourister, Lipault and Kamiliant in Malaysia

- Marks the Group’s entry into the Travel & Lifestyle e-commerce sector

It has signed an agreement with Samsonite Malaysia Sdn Bhd (“Samsonite Malaysia”), a wholly owned subsidiary of Samsonite International SA (“Samsonite International”), the world’s largest luggage manufacturer, extending the Group’s burgeoning portfolio of over 270 brand partners, which has surged more than 45.2% since 2017.

Through this agreement, Synagie will assist in the management of the online sales of Samsonite International’s brands including Samsonite, Samsonite Red, American Tourister, Lipault and Kamiliant across leading e-commerce platforms – Lazada, Shopee and Zalora in Malaysia. The Group’s integrated platform will enable Samsonite Malaysia to engage online effectively, by managing or automating its e-commerce process. The onboarding of Samsonite Malaysia as one of its brand partners, marks the Group’s foray into the Travel & Lifestyle ecommerce sector, further diversifying the Group’s potential revenue streams from the region.

Executive Director of Synagie, Ms Olive Tai commented, “We are truly honoured to be awarded with this opportunity to work with Samsonite, the world’s largest luggage manufacturer. It is a continued testament to the trust and faith that established brands entrust in us, as well as an affirmation of our ability to help businesses shift online and meet consumers’ needs. We will continue our momentum to buttress our leadership position in the e-commerce enablement sector in Southeast Asia.”

GEM FEATURE: HIGHLIGHTS FROM BERKSHIRE HATHAWAY ANNUAL MEETING

1) Buybacks: Berkshire repurchased $1.7b worth of shares in 1Q19 (more than 2H18), as its cash pile continue to swell to $114b. “We are going to be more liberal when it comes to repurchasing shares…we are certainly willing to spend $100 billion [on buybacks]” should Berkshire’s market value falls below intrinsic value

2) Amazon is a ‘value’ bet: Amazon rose on Friday after Buffett say Berkshire has been buying Amazon, although the decision was made by “one of the fellows in the office that manage money”, who took into consideration a slew of financial metrics. “The considerations are identical when you buy Amazon versus … say a bank stock that looks cheap against book value or earnings of some sort,”

3) Overpaying for Kraft Heinz: Heinz was at one-point Berkshire’s most valuable common stock investment but had lost more than 60% of its value since start of 2017, and recently delayed its 1Q earnings due to accounting issues. “Kraft Heinz is still doing very well operationally… I think the problem was that we paid a little too much for the last acquisition…. You can turn any investment into a bad deal by paying too much”

4) Caution on private equity: “We have seen a number of proposals from private-equity funds where the returns are really not calculated in a manner I would regard as honest….I would not get excited about so-called alternative investments.” It was recently reported that Buffet ‘looked’ at Uber investment 18 months ago, but passed. Uber is set to go public this month with a valuation of $83.8b on the high end of that range. Uber last raised money in the private market at a $76 billion valuation.

5) Berkshire after Buffett: At the CEO level, Berkshire has made Ajit Jain and Greg Abel vice chairmen, a move that was confirmed to be part of the succession plan. Jain oversees the conglomerate’s insurance businesses while Abel oversees non-insurance business operations.

How to get free upgrade to Business and First class or travel for free?

Bag the Air Miles

The simplest and most effective way to upgrade any plane ticket is to use airline miles. Some airlines (Example: Singapore Airlines) only allow you to jump one cabin, while others, such as Virgin Atlantic, will allow you to go all the way from economy to First class. An upgrade to a destination such as New York will generally cost between 50,000 – 80,000 airline miles each way.

And for the pessimists out there, airline miles are surprisingly easy to collect, even without flying. Singapore Airlines, Virgin Atlantic and others allow you to earn points for any shopping via their retail and F&B partners.

Bid your way up

Some airlines use upgrade system called PlusGrade to offer upgrade auctions. Customers on airlines such as Qantas, Virgin Atlantic, Lufthansa, Singapore, Cathay Pacific and many more allow you to bid for the luxury life up front. Simply login to your booking online and look for an offer to bid on an upgrade. If you can’t find it, simply google: “(Your Airline Name Upgrade Auction)”.

It’s important to keep a level head while participating in these auctions, since winning bids can occasionally exceed the price of just paying for business class from the start. Nonetheless they offer great value. Other airlines, such as British Airways and Emirates are known to flash upgrade offers in their mobile app. After making a booking, remain on the lookout for exclusives upgrade offers, some of which can be very attractive. We were recently offered a $400 one-way upgrade from Economy to Business class with Qatar on a flight from Singapore to Barcelona.

Find Great Deals!

Some Airlines business class flash sales. The very best flash sales are almost never officially announced, last mere hours and are gone before many travellers have had a moment to glance at their computer. Qatar Airways sold S$3,200 return business class seats from Singapore to Amsterdam earlier this year.

Gem News 18- Credit Card miles